1. Why is There Renewed Interest in India in 2014?

Despite growing at a faster pace than most of its large emerging market peers for the past decade, India has not experienced the hype around its growth prospects from the global community as it is facing now, with the country’s newly elected Prime Minister, Narendra Modi, conducting individual meetings with the heads of the three largest economies in the world. After sending the incumbent Congress home with its worst ever defeat since the party’s formation post India’s independence in 1947, Modi has managed to secure a nuclear deal with Australia, more than US$32 billion in loans and investments from Japan, another US$20 billion from China, and will be now making his way to the United States to woo President Obama.

2. How Does India Compare To Other Large Emerging Markets?

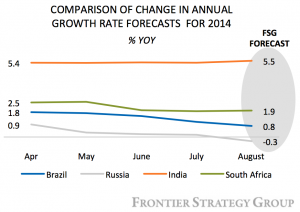

India is not only getting a lot of media attention due to the political and economic ties it is forging with the global giants but also due the bottoming out of its decade low economic growth rates. Recording a growth rate of 5.7% in the first fiscal quarter for 2014, its fastest in two-and-a-half years, has attracted plenty of MNC attention toward India. While the figures shouldn’t surprise you, because India was expected to grow between 5.5%–6% in FY2014, it is the relative performance of the country that has shifted investor attention; India’s peers Russia and Brazil are going through technical recessions, South Africa will see a sub less than 2% expansion, and China is also likely to grow at a slower pace than initially forecasted. While the Modi government is unlikely to have had any direct impact on the Q1 growth figures, the BJP’s impending victory would have played a significant role in the uptick. (click hereto see deeper analysis on India’s recently performance and how it affects your industry)

3. What Does FSG Mean by the ‘Modi’s September of Courtship’?

September began with Prime Minister Shinzo Abe pledging US$480million in infrastructure loans along with over US$32 billion of public and private investment and financing to India over the next five years. This was immediately followed by Prime Minister Tony Abbott visit to India where he announced the finalization of a deal that would allow Australia to export uranium to India for usage in civilian power plants. India then attended the ASEAN-India Summit where the eagerly anticipated free trade agreement (FTA) in services and investments was signed with the 10 nation ASEAN bloc, bringing India closer to becoming an integral part of the Regional Comprehensive Economic Partnership (RCEP – click here for a detailed report on RCEP). Following this progress, Chinese President Xi Jinping visited India and pledged US$20 billion in investment, focused on industrial parks and infrastructure, over the next five years to narrow India’s largest trade deficit with any single country (click here for details on Chinese investments and trade with India). Now Modi is making his way to the United States, where experts are expecting progress on the Indo-US defense cooperation, with the world’s two largest democracies likely to renew their security collaboration framework. (India’s exports to the United States have grown at an annualized rate of more than 12% over the past decade)

4. What Should You Expect From India Over the Next Six Months?

Given that the BJP holds a strong majority in the lower house and the first fiscal quarter performance has outperformed expectations, companies can expect India to grow at a faster pace in 2014 than it has over the past two years and experience a gradual recovery. However, annual plans shouldn’t assume strong Q1 figures to signal much stronger expansion in the rest of the year (i.e. double-digit growth); recovery will be gradual, and inflation will continue to put pressure on consumption, which accounts for 62% of the country’s GDP. India might also face some power issues this summer; 56 of India’s 100 coal-fired power stations have enough fuel for less than a week, putting India in a perilous situation. With demand rising because of a prolonged summer and lack of growth of supplies from domestic mines, companies could face power shortages along with another blackout, similar to the massive one seen in 2012 that put almost 600 million in the dark.

Consumption is expected to grow at a faster pace in FY 2014 compared to FY 2013, when it grew by 4.9%. Estimates for India’s Q1 performance indicate that private consumption grew at a healthy pace of 5.7% and continued to contribute to over 60% of the GDP. FSG continues to expect India’s GDP to grow at 5.5% during the FY2014-15 (on the back of improvements in spending and investments) and would recommend companies to hold-off on any upward adjustments until the BJP government begins to roll-out its reforms during the winter-session of Parliament (Nov-Dec 2014). The Indian Rupee has strengthened considerably over the past 10 months, on the back of an improving current-account-deficit and inflow of foreign portfolio funds. FSG expects the rupee to remain around its current-level, 59-61 rupees per dollar (the rupee averaged at 58.5 in 2013), for the rest of this year.

5. What Are We Telling Our Clients?

India’s private sector is optimistic and confident about the new government’s ability to pass reforms. Forecasts for the Indian rupee have improved (for the end of 2015) more than for most emerging-market currencies, and the benchmark stock index has climbed over 20% in value. While it is fair to be optimistic about the growth prospects, FSG believes that companies should remain cautious as many of the major fundamental changes that India needs to achieve its true potential have still not been announced (click here to see details on the fundamental changes needed for a total recovery). It is important to remember that back in 2010, former Chinese premier Wen Jiabao signed pacts valued at US$16 billion, including US$10 billion in equipment sales to three India power plans, of which, only one plant has been commissioned while the others are stalled due to lack of fuel and land permits.

FSG clients can access our Q3 India Quarterly Market Review on the client portal. Not a client? Contact us to learn more.