This post is part one of a 3-part blog series.

While the death of the emerging markets growth story is exaggerated, multinationals are clearly changing the way they are approaching the emerging market opportunity. This change became evident during FSG’s latest Senior Executive Roundtable on Oct. 7 in London. This event brought together more than a dozen regional presidents and heads of Europe, Middle East and Africa for an exchange in tactics and best practices from across industries and an interactive discussion to support their 2016 strategic planning.

Three priorities became evident during the event and have been further confirmed by regular discussions we hold with our broader client base. Follow this blog series to find out what these are and, more importantly, what multinational companies are doing about them.

Priority #1: Re-think your regional portfolio of markets

The sharp drop in commodity prices, acute currency volatility, and a variety of government reactions to these have created a new set of winners and losers across the region and dimmed the immediate growth prospects of a number of key EMEA markets. As a result, multinationals are looking to re-think where the opportunity is going to be for their business in the next one to three years, and which markets can help to compensate for weakness in some of the key regional drivers such as Russia, Turkey and South Africa.

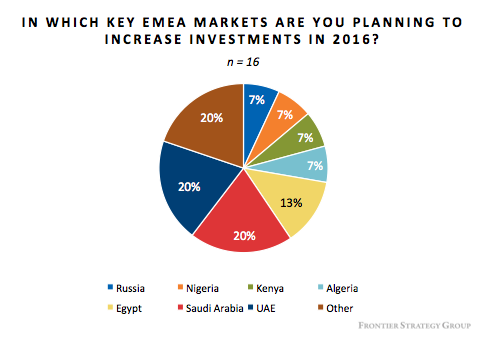

A few prioritization trends emerge when working with clients to help them build prioritization models while taking into account leading indicators of demand and (more recently) resilience. First, GCC markets are at the top of the agenda because of their perceived political and financial stability, especially in pegged currencies, as well as strong purchasing power. This is likely to lead to increased competition in these markets as most multinationals were planning to further increase investment there. This also means there is a risk of MNCs having overly aggressive targets for GCC markets at a time when they are dealing with low energy prices and looking to trim government spending.

Second, multinationals are in search of pockets of opportunity – markets that may be small but have big potential and are growing quickly with more limited multinational competition. Such markets include East Africa (especially Kenya), Iran, Egypt and Algeria. One such region to which multinationals are not paying sufficient attention is Central Europe, which is exhibiting relatively healthy growth and has been mostly spared by the deep currency depreciations that have decimated once-promising CIS markets.

Third, the big markets remain a priority, but profitability expectations are changing as currency depreciation erodes margins. Most multinationals have businesses in these countries that are so large that pulling back is not an option. These markets, however, may receive less new investment and will be under significant pressure to optimize operating costs. Russia, South Africa, Nigeria and Turkey are, not surprisingly, among them. Until the recent election results, Turkey in particular was a source of frustration for many of the executives in the room, as the constant currency depreciation and political uncertainty obscured the country’s growth prospects. A third of the executives in the room were planning to de-prioritize new investment in Turkey or freeze any investment plans for the next twelve months. This may not necessarily change even with the AKP’s strong election performance, but the country will certainly be worth a second look before 2016 strategic plans are finalized.

Our next two posts will cover the other two priorities for multinational executives heading into 2016: reshaping the value proposition and optimizing distribution networks.

To learn more about FSG’s EMEA Senior Executive Roundtable, please listen to our podcast. Not a client? Contact us to learn more.