Despite Latin America’s notorious economic slowdown during the last couple of years, Colombia has emerged as one of the top performers in the region and the second most important market for investment for 31 percent of multinationals (according to a recent poll conducted by FSG). As companies seek to enter Colombia or expand their presence in the market, they are confronted with two main challenges related to their go-to-market strategy: (1) deciding between the most favorable distribution models that include direct, indirect and hybrid distribution and (2) structuring a solid channel management process in a way that maximizes market share and profitability over the long-term.

In an effort to help clients effectively tackle these and other challenges related to channel strategy in Colombia, Frontier Strategy Group has developed a report for clients that presents key processes, factors and best practices that companies should take into consideration as they make key decisions related to channel design and channel transitions in the Colombian market.

Below are the key processes that companies will need to get right to succeed in the Colombian market:

1) Decide the best and most feasible distribution model (direct vs. indirect) for your company

To do so, companies will first need to conduct a self-evaluation of their short and long-term targets, the level of capital to be committed for the new endeavor, their level of market knowledge, and the level of sophistication of the products they want to sell (company factors). Additionally, companies will need to make a thorough assessment of Colombia’s characteristics in terms of client size and dispersion, operating environment, bargaining power of potential partners, and competitor strategies (market factors).

Company factors

- Sales growth horizon/ short-term versus long-term targets

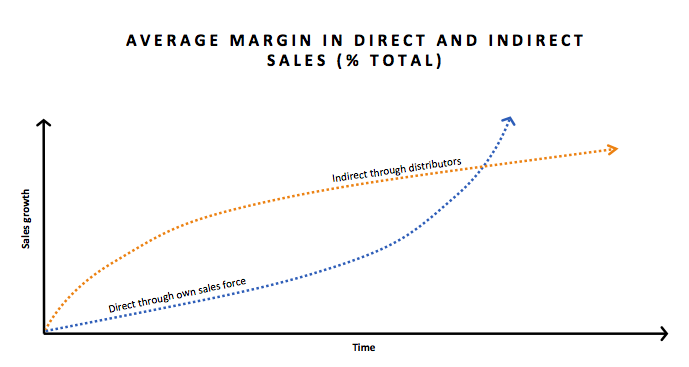

Multinationals should carefully evaluate the pros and cons of selling their products through direct or indirect distribution models, taking into consideration their sales targets and the time that it takes to achieve those targets. For example, an indirect model could generate faster sales growth in the short-run, but it could also imply a lack of control over the sales process, which may hinder long-term growth.

- Capital commitment

High operating costs, stemming from the poor logistics infrastructure that connects Colombia’s main consumption centers, make direct distribution a very expensive option for many multinationals. However, despite the higher capital commitment required to deploy a direct sales model, companies with enough financial support from corporate may want to proceed with this option. This is because the upside opportunities associated with full control of the sales force and processes, direct interaction with key clients, and the possibility of more solid growth over the medium- to long-term can outweigh the upfront costs.

- Market knowledge

Market knowledge and experience play a key role to succeed in Colombia, as ease of doing business may vary significantly from one city to the other. As such, multinationals need to conduct a self-assessment of their market knowledge against that of potential partners (distributors) as they try to expand into new customer segments, or into Tier 2 and Tier 3 markets.

- Product sophistication

The choice between direct and indirect distribution may be constrained for companies that sell very sophisticated products as the country suffers from significant talent shortages affecting key areas for business development, particularly in high-tech sectors. This fact is highlighted in FSG’s most recent client survey that touches on talent recruitment and retention challenges in Latin America. As such, companies selling highly sophisticated products might need to invest in developing and training their own sales force.

Market factors

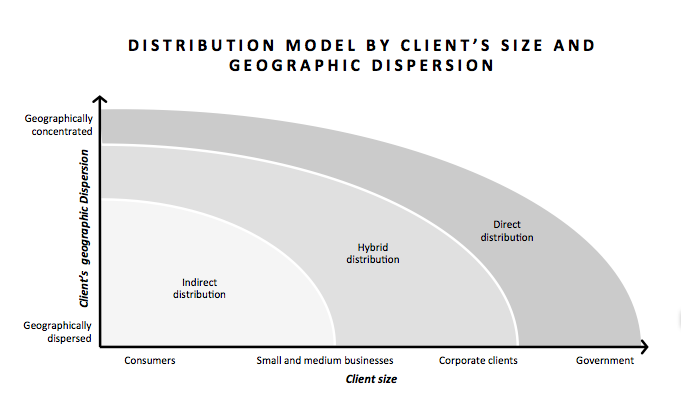

- Client size and geographic dispersion

Companies whose potential clients are highly concentrated in specific cities or regions should consider entering Colombia through direct distribution, as logistic costs per unit sold are likely to be low. On the other hand, since logistics costs associated with nationwide coverage tend to be higher in Colombia as a result of the country’s poor infrastructure, companies with more geographically dispersed clients should consider using distributors as a way to achieve a wider reach in a more cost-effective manner.

- Operating environment

In many cases, Colombia’s complex operating environment can make direct distribution models overly expensive for multinationals. For example, companies selling big-ticket items, particularly in the technology and healthcare sectors, will need to incur an extra costs related to cargo insurance and security escorts, as trucks carrying products outside Colombia’s main urban areas are highly vulnerable to merchandise theft. As they choose between direct and indirect distribution, these companies will need to ask themselves whether they can run logistics more efficiently than other more established distributors with national coverage.

- Distributor bargaining power

Working with consolidated distributors in Colombia is costly, as their expertise in managing the market’s complex business environment, coupled with the increasing influx of FDI into the country, has tilted bargaining power in their favor. As such, multinationals that hope to partner with competitive distributors must sacrifice more margin – approximately 30 percent – relative to the regional average of 24 percent. As a result, some companies either decide to deploy a direct sales model or partner with and invest in smaller distributors to help them become larger and more competitive.

- Competitors’ strategies

Competitors’ channel structures could limit available strategies for new entrants. If competitors are using direct sales for specific segments or markets and margins are low, companies will find it hard to offer competitive prices through distributors. Also intense competition for the strongest distributors sometimes leaves only smaller or less competitive distributors available.

2) Structure a solid and feasible channel management process

Once the best distribution model has been defined, it is critical for companies to design and structure a solid channel management process, as failure to do so could lead to significant sales underperformance. As such, multinationals need to take the time to identify the most feasible best practices to make sure their channel partners are developing the capabilities that will allow them to deliver healthy sales growth over the long-run, while also swiftly adapting to any sudden market change. In our report, we identify four key best practices that will help multinationals to build a robust channel management process to support the continued improvement of their channel partners and drive sustainable long-term growth:

- Create weighted scorecards that measure capability inputs as well as commercial outputs

Use a weighted performance scorecard that measures both commercial outcomes and capabilities, as there is often misalignment between what multinationals need from partners and what they measure, and the fact that channel managers often place too much emphasis on commercial outcomes rather than on capabilities that drive long-term growth.

- Use an easy-to-understand incentive structure to maximize performance

Reinforce capability development with variable compensation schemes tied to your weighted performance scorecard. Tying your performance-based incentives directly to the weighted scorecard results is a good way to reinforce capability development. Additionally, rewarding partners with status, rather than just margin, helps partners to understand exactly where they stand versus other distributors.

- Support your partners by using a customized management calendar

Support partners by creating a robust management calendar that reinforces information-sharing expectations and capability development. A robust calendar of interactions with partners throughout the year will not only support accountability and compliance, but most importantly, it will support capability-building and will drive consistent long-term performance.

- Provide appropriate resources to upgrade your own internal capabilities

Support partner development by providing channel management teams with capabilities that fulfill the unique demands of the distribution manager role. In many companies, channel managers often rise through the sales organization, which leads to capability gaps that arise from misalignment between sales management skills and channel management skills. Multinationals should evaluate the roles, responsibilities, hiring profile, and professional development needs of channel managers within the organization, recognizing that great sales skills alone will not make someone a great channel manager.

As companies look to expand their presence in the Colombian market, getting channel strategy right will be key for success, especially as competition intensifies on the back of higher investment from corporations that see Colombia as one of the few remaining pockets of opportunity in Latin America. In this respect, and for better or worse, sales through distributors currently account for 75 percent of multinational’s revenues in Colombia.

For an in-depth analysis of this topic, FSG clients can access the full report on the client portal. Not a client? Contact us to learn more.