The March 4 U.S. jobs report was exceptionally strong and should be viewed as evidence that financial markets under-appreciate the case for further monetary tightening. With a FOMC meeting this week, financial markets run the risk of being caught on the wrong foot by an unexpectedly hawkish Fed. FSG believes that given the stated parameters that inform Fed decision making – namely stable prices and full employment – the recent report provides little reason for the central bank to diverge from its publicly stated course of monetary tightening. The growing incongruity between the market’s dovish expectations and the strong economic data that informs Fed decision-making points to a potentially rude awakening for financial markets and the threat of greater market volatility.

It’s about data, not sentiment

The Fed has always used data as an essential input to its policy decisions. However, the central bank’s turn to “data dependency” as a form of forward guidance shifted financial market attention to domestic economic reports such as the U.S. Current Employment Statistics (the “jobs report”) to try to uncover signals for when the Fed might move next. Fluctuating market sentiment might occasionally cloud the picture, but it has remained important to keep key economic data in mind when evaluating future Fed policy.

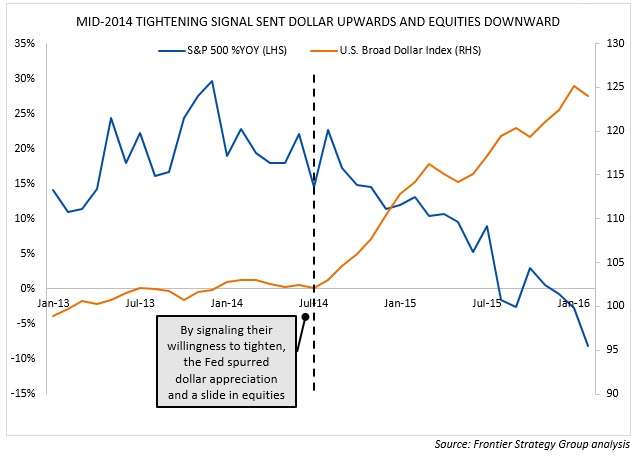

The Fed first made its move to “data dependence” in its June 2014 meeting. By stating that its first rate increase since 2006 would be, “a decision that will depend on the Committee’s evolving assessments of actual and expected progress toward its objectives,” the Fed telegraphed the message to financial markets that maintaining the federal funds rate at the “zero lower bound” was no longer a policy objective. Instead, economic data regarding the Fed’s dual mandate – full employment and a 2% inflation target – would inform its monetary policy decisions. While this may seem uncontroversial, it represented an important shift for a central bank that had pursued monetary policy easing as a matter of course. It also represented the first potential shift to a policy of active tightening since the financial crisis. This announcement sent shock waves throughout the financial system, slowing the growth of equity markets to the point of eventual contraction, and sending the dollar skyrocketing.

The correction in equities and an increasingly strong dollar soured the mood on Wall Street and in Corporate HQs across the U.S., as the international earnings of the companies that populate major indices plunged. The impact of the strong dollar is of course very significant for multinationals and portfolio managers, but this focus on exchange rate has unduly colored market sentiment. The dollar’s impact on U.S. economic fundamentals is limited, yet the appreciation of the dollar and the drop in earnings that resulted has prompted market participants to under-price the risk of further tightening. But if we strip back the emotional drivers of this negative sentiment, we see the economic data in the recent jobs report makes the case that additional tightening is far from the remote possibility that markets indicate.

February jobs report is an unambiguously positive signal for “data dependent” Fed

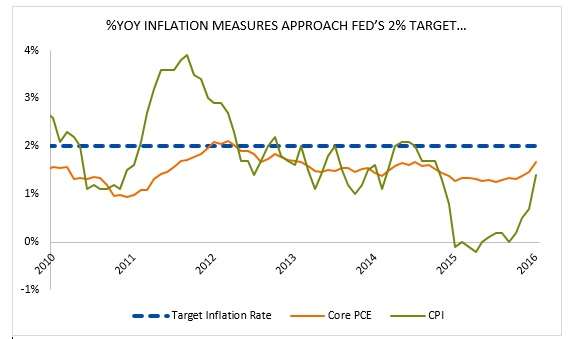

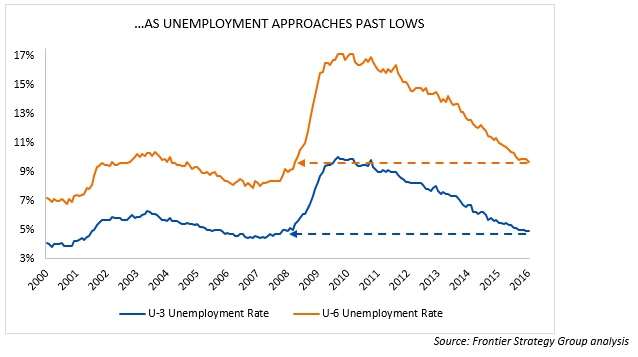

The headline returns of this month’s job report were unambiguously positive. First, Nonfarm Payrolls significantly beat analyst estimates, posting a gain of 242k vs an estimated 195k and core inflation (all items less food and energy) grew 0.3% month-over-month. These gains in employment and price levels occur in a context of unemployment measures approaching past lows and inflation nearing the Fed’s 2% target (see graphs). Of equal importance are the upward revisions to initial job gain estimates of the December and January reports, which were bumped upwards from 262,000 to 271,000 and 151,000 to 172,000 respectively. These revisions demonstrate the continued strength of U.S. labor market gains and should fuel further skepticism regarding the market’s recent bout of pessimism.

While such numbers give strong indication that U.S. domestic economic conditions are improving in a manner consistent with a course of further rate hikes, one piece of the puzzle still appeared to be missing. Wages – growth of which would indicate a tightening in the labor market consistent with full employment – actually decreased 0.1% month-over-month, suggesting (somewhat improbably) that employment slack still exists and the long-term path of inflation – usually fueled by the increased purchases that result from improved wages – will remain subdued.

Reaction to the report centered on its wage data, as it seemingly belied the otherwise clear picture of continuing economic improvement painted by the release. However, FSG believes that this wage data needs to be viewed in its full context to be appropriately understood, as a quirk in the numbers indicates that wage growth may not be as subdued as it seems.

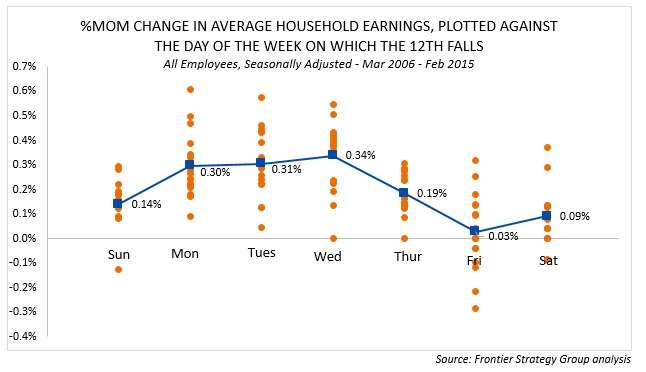

In fact, the “bad news” on wage data is largely a statistical fluke. Because the B.L.S. collects data for the jobs report on the 12th of each month, the day of the week the survey is administered varies from month to month. In theory, the day of the week on which data is collected should not have an effect on the economic information produced. But a pattern emerges when plotting all month-over-month wage growth data points since 2006 based on the calendar day the 12th falls on:

For ambiguous reasons related to the methodology and construction of the survey, the numbers collected on Friday are reliably lower than those collected on other days. In fact, wage growth data collected on Fridays historically posts the lowest average month-over-month growth of all days of the week. Additionally, data collected on Friday has resulted in the largest number of historical month-over-month contractions, a fact that casts the recently measured contraction in wages in a much different light. The calendar effects of this wage measure is appreciable, as FSG’s statistical analysis attributes over 40% of all variation in historic month-over-month wage growth to the day of the week on which the 12th fell on.

What to expect

Markets jumped on the recent wage numbers as evidence that corroborates their overly dovish view of future Fed policy. If lackluster wage growth was the only issue that held up last Friday’s jobs report from being interpreted as clear support for further rate increases, our analysis demonstrates that this argument is less convincing than it initially appears. The significance of this potential misalignment is as follows:

- If hawkish projections for a rate hike emerge from the FOMC minutes this Wednesday, financial markets run the risk of being caught by surprise. Hawkish forward guidance would boost the dollar, the appreciation of which has slowed to a standstill since the start of 2016

- Resulting currency volatility will continue to slam the earnings of multinationals with established presences in Emerging Markets and weigh on U.S. exports

- Given the depth of the easing policies that other major central banks are pursuing, such as the BOJ and the ECB, monetary policy divergence and central banks will continue to drive the macro cycle

- For better or for worse, markets drive sentiment. The since-recovered downturn in U.S. equities that started the year prompted conversations of whether the U.S. was on the verge of recession. While the fundamentals point nowhere near this, overly negative sentiment can sometimes become self-fulfilling, a needless risk to global growth if markets are not careful

For our latest updates and insights, FSG clients can visit the client portal. Not a client? Contact us to learn more.