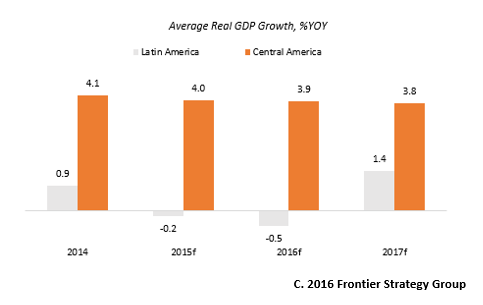

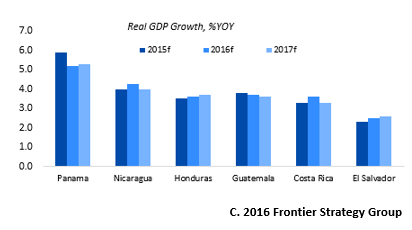

While Latin America is expected to contract by 0.5% in 2016, the Central American sub-region will grow by almost 4%, situating itself among the best performing markets globally. However, economic performance is expected to vary significantly across the markets in Central America, with highest expectation for economic growth in Panama, and lowest in El Salvador.

Drivers of Growth in Central America

Higher growth in Central America, relative to the rest of the region, stems from two factors: first, the strong economic ties of the sub-region with the US and, second, its heavy reliance on energy imports. This was once a curse when oil prices were topping $140 USD per barrel by 2008, but has since become a blessing for governments and consumers across markets.

Despite this, the US continues to drive most of Central America’s growth. The normalization of monetary policy in the US and expectation of at least two additional interest rate hikes this year by the Federal Reserve will, in theory, reduce capital flows to developing countries. However, this effect will be less felt in Central America than in the rest of the region. This is largely due to the acceleration of consumer spending in the US as a result of a stronger labor market, and steady increase in wages which is expected to: (i) boost Central American exports; (ii) raise remittances, and (iii) boost tourism spending.

Markets that stand to benefit the most from their commercial ties to the US are Nicaragua (52% of exports to the US), El Salvador (47%) and Costa Rica (38%). Guatemala, Honduras, El Salvador and Nicaragua will also benefit greatly from higher remittances as the job market in the US recovers. Lastly, increased tourism spending will support growth, especially in Costa Rica, Panama and Nicaragua.

Key Highlights by Market

High Performers: Costa Rica and Panama

Panama and Costa Rica are expected to remain top priorities in the region, and together already boast the largest share of Foreign Direct Investment into Central America. In the case of Panama, focus is placed on its faster headline growth, whereas in the case of Costa Rica, the focus is on strong consumer demand driven by high per capita income and steady political and macro situations.

Panama

Panama’s economy represents over 20% of Central America’s GDP and, while its growth rate has been slowing, Panama’s economy continues to grow faster than the rest of the region. It will remain the fastest-growing economy in Central America, with expected growth above 5% through 2017.

Significant public and private investments in the Panama Canal extension, which is expected to yield increased revenue, will increase shipping capacity by as much as 100% and lead to sustained economic growth. Even when construction works are over, Panama’s growing participation in global commerce and role as a logistics hub for the region should continue to support high growth in the country. In fact, MNCs in various industries have already sought to establish regional headquarters, shared services centers, and logistics hubs in Panama.

The Panamanian government is also expected to remain pro-investment as the economy’s growth becomes increasingly dependent on the continued expansion of the services sector, which relies upon growth in the logistics, transportation, and financial services sectors. Additionally, falling unemployment, rising wages, and an increasingly affluent population have contributed to stable consumer spending and retail development in the past decade. Lastly, the Panama Papers, which brought to light the country’s participation in moving and hiding illegally sourced funds, will likely drive governments to scrutinize more closely business operations by MNCs operating in the market, and encourage genuine financial growth and stability.

Costa Rica

Costa Rica remains an attractive market with one of the most highly developed economies in the region, low levels of violence, and political stability. Comprising nearly 25% of Central America’s economy, Costa Rica is expected to grow below 4% over the short- to medium-term due to a growing service sector, which remains a significant focus of investment.

While fiscal challenges may be curbing potential growth and tempering investment enthusiasm, the Costa Rican economy has experienced consistent and stable growth in the past decade and continues to attract significant FDI. In particular, the country’s service sector, which now accounts for over 70% of Costa Rica’s GDP, will lead economic growth, while exports and tourism are expected to be bolstered by US growth and recovery. Additionally, Costa Rica is endowed with a skilled and very well-educated workforce, which furthers the country’s attraction for establishing shared services and research & development centers.

On the negative side, increasing input costs and concerns over tax policy have hindered the country’s upside potential. Its structural fiscal deficit has yet to be successfully addressed, as the government exhibits reluctance to pursue tax increases over the short- to medium-term, despite running significant fiscal deficits in recent years. As a result of the lack of fiscal discipline, the IMF has insisted that Costa Rica raise overall tariffs in order to stabilize its debt-to-GDP ratio. This could lead to an inevitable increase in taxes and downward pressure on disposable income in the short-term, as well as the removal of tax incentives on FDI in the medium-term.

Come back next Tuesday, May 10th for an update on Central America’s laggard and rising star markets, as well as actions for your business to take to refine your Central America strategy.