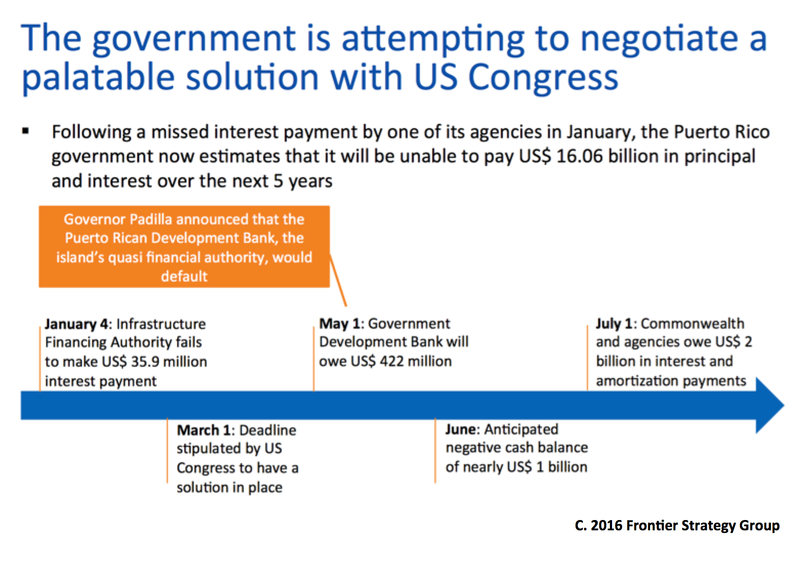

Only three weeks after passing a debt moratorium law, the government of Puerto Rico has defaulted on the debt of the island’s Government Development Bank. In doing so, it has essentially chosen to prioritize current spending on key social services, rather than service its interest and amortization payments that fell due on Sunday, May 1st.

The decision follows months of negotiations in the US House of Representatives where lawmakers have attempted to cobble together a deal that would facilitate the restructuring of Puerto Rico’s nearly US$70 billion in debt, while also providing a federal oversight board to insure the island puts its fiscal house in order. Despite significant efforts, due to disagreements around key terms of the agreement, final legislation has yet to be produced. As such, Puerto Rico has been left with little recourse but to default.

Puerto Rico now faces a new deadline of July 1st, at which point it will see approximately US$2 billion of interest and amortization payments come due. Importantly, of this US$2 billion, US$800 million is general obligation debt. This means that its repayment is constitutionally guaranteed, and the consequences of non-payment would be much more severe for Puerto Rico’s finances, as well as the larger municipal bond market.

Immediate effects on business:

- Government spending (negative): The Puerto Rican government already delayed payments to key suppliers and cut dispensable outlays (such as reducing the number of schools) prior to this default. However, the government is expected to experience a US$1 billion budget shortfall by June, which would necessitate further cuts, delays, or both. In this regard, multinationals should look to hedge against any exposure to partners or customers that do business with the Puerto Rican government.

- Consumption (flat): In the short- run, expect little change in terms of private demand from the island. While the public sector wage bill has risen in recent years, it is unlikely that the government will make the unpopular move of enacting layoffs in the short-run. Meanwhile, the private labor market, where participation rates have fallen below 40% (compared to 63% in the US), is unlikely to deteriorate further in the short-run.

- Investment (flat): Investment in the island was already largely stagnate, as business leaders waited to see the result of the negotiations surrounding potential debt restructuring. While tensions have risen, expect investment conditions to show little material deterioration or improvement until we arrive closer to the July 1st

- Financial sector stability (flat): Puerto Rico’s commercial banks have little exposure to the Development Bank’s debt, and relatively high capital ratios. However, Puerto Rico’s cooperative savings institutions were owed approximately US$48.5 million on May 1st. Fortunately, in order to limit the impact of non-payment, these banks were already able to trade their bonds for bonds maturing in May 2017.

Looking ahead

- June 1st deadline: As mentioned previously, the July 1st deadline will be a major factor in determining the direction of the Puerto Rican economy in the medium-term. Without some sort of debt renegotiation prior to July 1st, Puerto Rico would likely default on general obligation debt, the bond issue that was largely viewed by market actors as being fail-safe. In such a case, Puerto Rico could confront years of court battles with holdout creditors and a further loss of credibility, two events that would essentially serve to lock the island out of international capital markets for the foreseeable future. This by itself would severely cripple the island’s finances, weighing heavily on consumption and investment. However, FSG still believes that both the potential humanitarian implications, as well as the implications for the US municipal bond market, will push the US Congress to action.

- Medium-term implications of a Congressional deal: Should Congress reach a deal before the July 1st deadline, which at this point will be difficult but not impossible, Puerto Rico will likely be able to quickly seek new funding to maintain essential services. That said, as part of the deal the island would also be required to submit to a federal oversight committee and enact significant new cuts while raising new revenue. In such a case, companies should expect to see new pressure on operations reliant on the public budget.

- Unfunded pension obligations: Aside from its US$70 billion in debt, Puerto Rico also has about US$45 billion in unfunded pension obligations. Even after arriving at a solution for its debt, Puerto Rico will necessarily need to reform its pension system, most likely cutting benefits and thus weighing on current and future consumption. This will be a politically contentious move, and would likely require some interference from the proposed oversight board.

Actions to take

Multinationals should continue to follow developments in the US Congress toward an ultimate resolution. Likewise, multinationals operating in Puerto Rico should assess exposure via channel partners or end customers to further payment delays or non-payments by the Puerto Rican government. Finally, multinationals with manufacturing operations on the island should assess how future reduced government spending and potential tax hikes would affect their operations, and whether these will continue to be competitive.

Because of its ties to the US, consequent high per-capita income, and draw as a tourist market, Puerto Rico will continue to be attractive for consumer goods companies. However, the long-term attractiveness of local manufacturing and the island’s ability to drive growth will be determined by the terms of the eventual solution.

For our latest updates and insights, FSG clients can visit the client portal. Not a client? Contact us to learn more.