Right now all eyes are on the conflict in Iraq. However, political instability is the regional norm, as seasoned senior executives can attest. Companies must avoid making rash decisions in response to regional volatility. Otherwise, there is a danger of cannibalizing long-term prospects for MENA growth.

Senior executives must be proactive in controlling the conversation with their corporate office to counteract the steady stream of negative media attention that is focused on the region. Despite the terrible human toll from the Iraq crisis, and increasing links to the devastating Syrian civil war, only 11% of MENA GDP is derived from markets that are highly exposed to spillover from the conflicts.

Senior executives should assess how deteriorating stability in Iraq impacts their MENA strategy, but a measured response is required. FSG suggests considering three actions for your regional business:

1. Course-correct your MENA strategy, but do not waste resources on a complete overhaul.

Risk-tolerant companies can gain long-term market share as others freeze investments or pull out of Iraq and surrounding countries. At the same time, MNCs can focus on a profitability-driven strategy in stable countries such as Saudi Arabia and the UAE. Our clients can use FSG’s market prioritization tool to aid in reassessing where to concentrate regional resources. They can also track signposts in our Iraq report and updates from FSG’s MENA Monthly Market Monitorto help decide when changes are appropriate.

2. Leverage local partners to maintain a foothold in affected areas in the MENA region.

Risk-averse companies can maintain a foothold in unstable markets by relying on local partners to reduce financial and security risks. It will be important to work with partners to monitor changing regional perceptions of Western brands if there is a sustained Iraq conflict in which foreign intervention is possible. Clients can review FSG’s Managing Distributors in MENA for additional strategies.

3. Count on de facto or de jure Kurdish independence, which brings opportunities and risks.

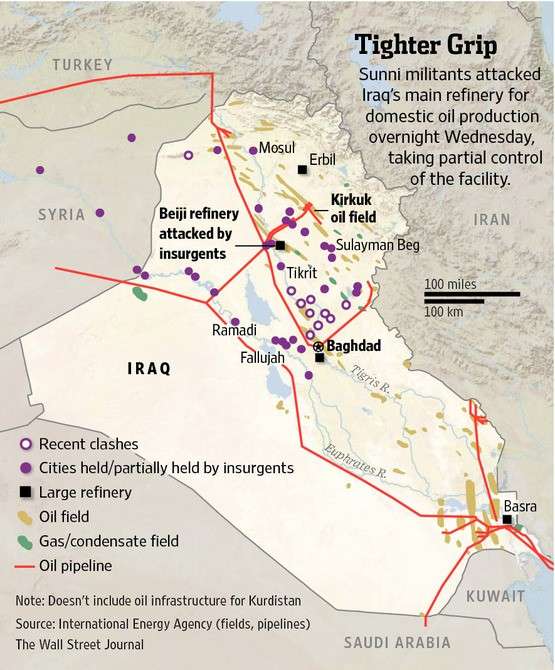

Kurdistan’s capture of oil-rich Kirkuk puts it on an accelerated path toward de facto or de jure independence. Kurdistan could become even more of an investment destination as a result. But manage expectations, as there are new challenges, including potential fuel shortages as a result of disruptions to the Baiji oil refinery and Erbil’s exposure to a rise in terrorist attacks. Clients can read our Iraq Frontier Market Access report for more on Kurdistan and use our monthly MENA report to track developments.

(Image courtesy Getty Images, Scott Platt: A Kurdish soldier with the Peshmerga keeps guard near the frontline with Sunni militants on the outskirts of Kirkuk, an oil-rich Iraqi city on June 25, 2014.)