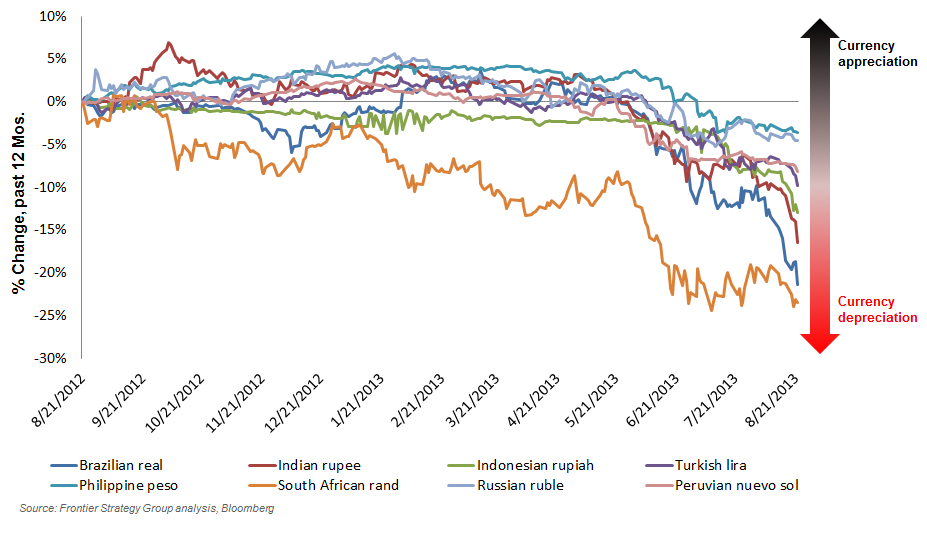

Recent reversals in capital flows caused large and sudden currency devaluations, faster than many emerging markets expected or could manage. As a result, many market commentators have called this end of the emerging markets opportunity. That statement couldn’t be further from the truth. While companies should always expect challenges in emerging markets, the changing environment will also create a new set of opportunities.

Recent reversals in capital flows caused large and sudden currency devaluations, faster than many emerging markets expected or could manage. As a result, many market commentators have called this end of the emerging markets opportunity. That statement couldn’t be further from the truth. While companies should always expect challenges in emerging markets, the changing environment will also create a new set of opportunities.

FSG identified four ways companies can capture growth in this shifting environment:

- Leverage home-currency strength to win share back from emerging markets–based competition

- Double down on local production to reduce production costs

- Use balance sheet strength to earn financing margins

- Reassess customer segmentation to identify local customer “winners”

FSG looks at these strategies and the drivers of the changing global environment in our 2014 Global Performance Drivers report, now available for FSG clients.

What happened?

Capital flows reversed because of push and pull factors. As the US economy continues to improve, the Federal Reserve is expected to reduce bond purchases, changing the risk-return payoff for portfolio investors, “pulling” capital out of emerging markets. We also see slowing growth in emerging markets “pushing” capital to developed markets. The outflow of capital is more concerning for countries like Turkey, Poland, and Ukraine, which have high levels of short-term external debt. Countries fitting this profile may run into short-term funding challenges that could drive up local interest rates, or in the worst case cause temporary liquidity problems. Other countries like India and Indonesia may now struggle with inflation as currencies decrease faster than is manageable, driving up costs for consumers.