LinkedIn

LinkedIn Twitter

Twitter

Getting the Right People in the Right Seats Has Never Been Cheap or Easy in Latin America

Even under the best of circumstances, it is difficult and expensive for multinationals to recruit and retain key talent in emerging markets. This is particularly true for the companies we work with in Latin America, given that governments across the region have historically under-invested in education and human capital. As a result, the supply of workers with the technical and managerial skills needed to carry out day-to-day business operations remains limited.

The underlying scarcity of skilled labor continues to drive up wages across the region, and in most cases, nominal wages outpace both inflation and productivity, boding poorly for the sustainability of current labor market dynamics and the consumption-led growth they have facilitated over the medium-term.

To make matters worse, demand for talent continues to rise as multinationals step up their investment in the region in an effort to compensate for sluggish growth in developed economies. Problems related to talent management have long plagued Brazil, and our expectation is that as companies strive to scale up their presence in Colombia and Peru, existing recruitment and retention challenges in these markets will be exacerbated, forcing companies to rely on costly expatriate hires.

Unfortunately, there is no silver bullet—today’s talent gaps are structural and will endure over the medium term even as governments begin to step up investment in secondary and tertiary education. However, conversations with our clients and expert advisors reveal that integrating workforce planning into the strategic planning process pays great dividends and helps companies move away from ad hoc, high-cost external hiring towards cost-effective, retention-boosting redeployment strategies.

Cost-effective Workforce Planning Is the Key to Unlocking Efficiency, Retention, and Revenue Gains

Redeploying internal talent more efficiently is a cost-effective near-term alternative to external hiring, while optimizing your regional organizational footprint offers a medium-term solution to the high costs associated with across-the board localization. Over the long term, hiring young and investing in top performers to ensure they gain the skills they need to assume leadership roles within the organization is the key to building a cost-effective, enduring talent pipeline with retention and brand building gains that compound over time.

The ability to redeploy existing talent is contingent upon increasing visibility into the internal labor pool. If visibility is a challenge, consider adopting programs aimed at increasing senior management’s exposure to high potential employees throughout the organization, across functional, geographic, and business unit lines.

Requiring senior managers to have succession plans in place, and ensuring that KPIs incentivize managers to develop their direct reports are two best practices for preventing managers from shielding their high performers in the hopes of keeping them on their teams to the detriment of broader organizational goals.

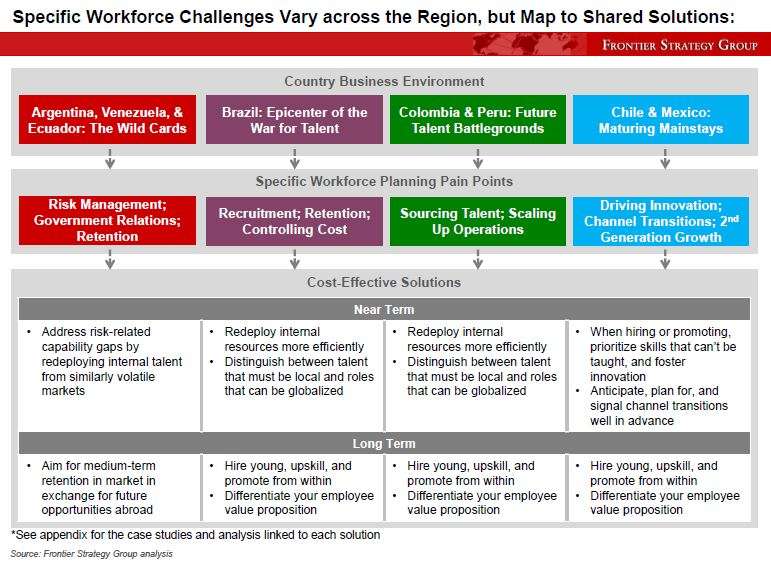

Additionally, grouping countries based on their business environments and labor market conditions allows you to leverage strategic economies of scale by prioritizing capabilities you need in each environment, cross-applying workforce planning best practices, and planning for the future as markets and competitive landscapes evolve.

One industrial company we work with offers a case in point: to mitigate the risks associated with heterodox macroeconomic policies in Argentina, their regional leadership team leveraged the expertise their Venezuela country manager had gained through years of navigating complex capital controls, high inflation, shortages, and retention challenges, and tasked him with strategic responsibility for Argentina. As ‘wild card’ manager, he was able to work with his Venezuela functional heads to quickly bring their Argentine counterparts up to speed on best practices for mitigating financial and operational risks.

There are benefits to be gained in extending this line of thinking to other types of business environments. For example, the workforce planning challenges that companies face today in Brazil are likely to be repeated down the road in Colombia and Peru as investment increases and subsequent demand for relatively scarce skilled labor accelerates. Internship programs and long-term investment in the training and development of local hires have proven successful in Brazil, and understanding common trends in labor market dynamics is essential to making the case for investing in similar programs in the Andean region, so that your company will be well-positioned to ride out the coming talent crunch.

For further reading on cost-effective workforce planning strategies and organizational footprint optimization in Latin America, FSG clients are encouraged to review the following reports:

- Click here to access our full report on cost effective workforce planning and regional labor market dynamics in Latin America