LinkedIn

LinkedInFrontier Strategy Group is witnessing a dizzying array of changes to the business landscape in Latin America. Some are highly visible shifts in the external political and economic conditions in key markets such as Brazil, Mexico, and Venezuela, to name a few, while others involve subtle evolutions in internal corporate mandates for Latin American business units of multinational corporations. For this reason, FSG recently released a new Regional Overview of the factors influencing the results of our clients as well as emerging trends likely to impact performance and shape strategy for the coming years. The research is drawn from extensive interviews with senior executives at leading multinationals, independent experts, and analysis of surveys of FSG’s client base. Below are featured trends from the report, accessible to FSG clients:

Economic Performance is Strong, but Risk - and Skepticism - is Growing

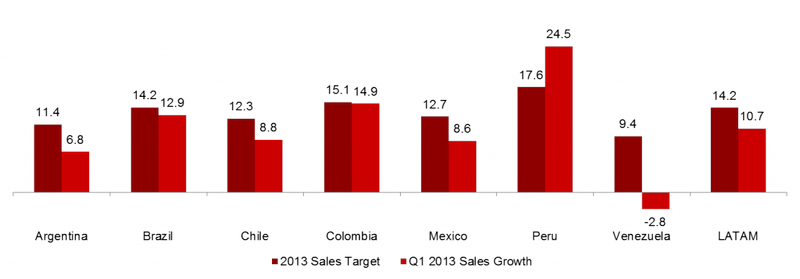

Compared to global averages, and even in comparison to other emerging market regions, Latin American growth remains, in the aggregate, relatively robust. Yet many industries in Latin America in 2012 either just met or underperformed expectations, and now with a persistent slowdown and protests in Brazil and crisis always on the horizon in Venezuela and Argentina, skeptics are growing louder, forcing executives to justify further investments in the region. Furthermore, FSG’s data indicates that slow growth in Argentina, a weak Q1 in Mexico, and the devaluation in Venezuela threaten goal attainment of sales targets in 2013 as well.

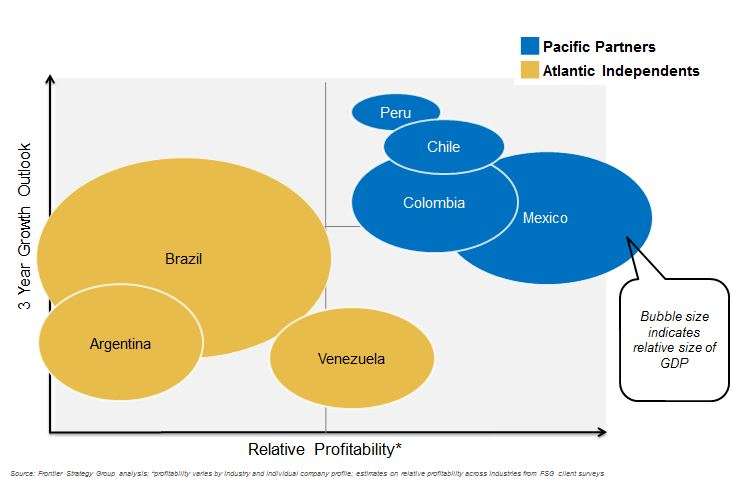

Latin America Splitting into Two Distinct Groups: Pacific and Atlantic

The dynamic Pacific economies are integrating rapidly, as evidenced by the creation of the Pacific Alliance trade group, creating new trade dynamics and opportunities for increasing scale and reorienting supply chains. In contrast, the Atlantic economies are increasingly insular and crisis prone, a trend typified by the increasingly dysfunctional Mercosur customs union. These distinctions are growing and becoming more tangible as companies position to mitigate risk from reliance on Mercosur and maneuver to gain from new opportunities presented by the Pacific Alliance.

The “Grow-fast, Worry about Profitability Later” Days are Coming to an End

Many executives perceive a strong shift in corporate mandates for Latin American business units towards bottom line results, rather than purely on top line growth. This shift is changing the way executives prioritize markets, evaluate organizational structures, measure and orient workforces, and make the case for resources.

New Blueprints for Success

As both internal corporate and external dynamics have changed, senior executives are drawing up new blue-prints for success by examining existing assumptions around optimal organizational footprints and structures and by prioritizing markets and communicate opportunity based new criteria such as relative profitability and operating margins.

Conclusion

FSG’s LATAM Regional Overview expands on these trends and shares analysis of client survey responses on how they are responding to these shifts. FSG believes that despite increasing volatility and growing macroeconomic and political risks, Latin America continues to offer excellent opportunities and high returns relative to other regions. That said, today’s business environment already is significantly different from that of just a year or two ago, and regionally-focused executives are wise to recognize that their strategies must evolve in tandem.