LinkedIn

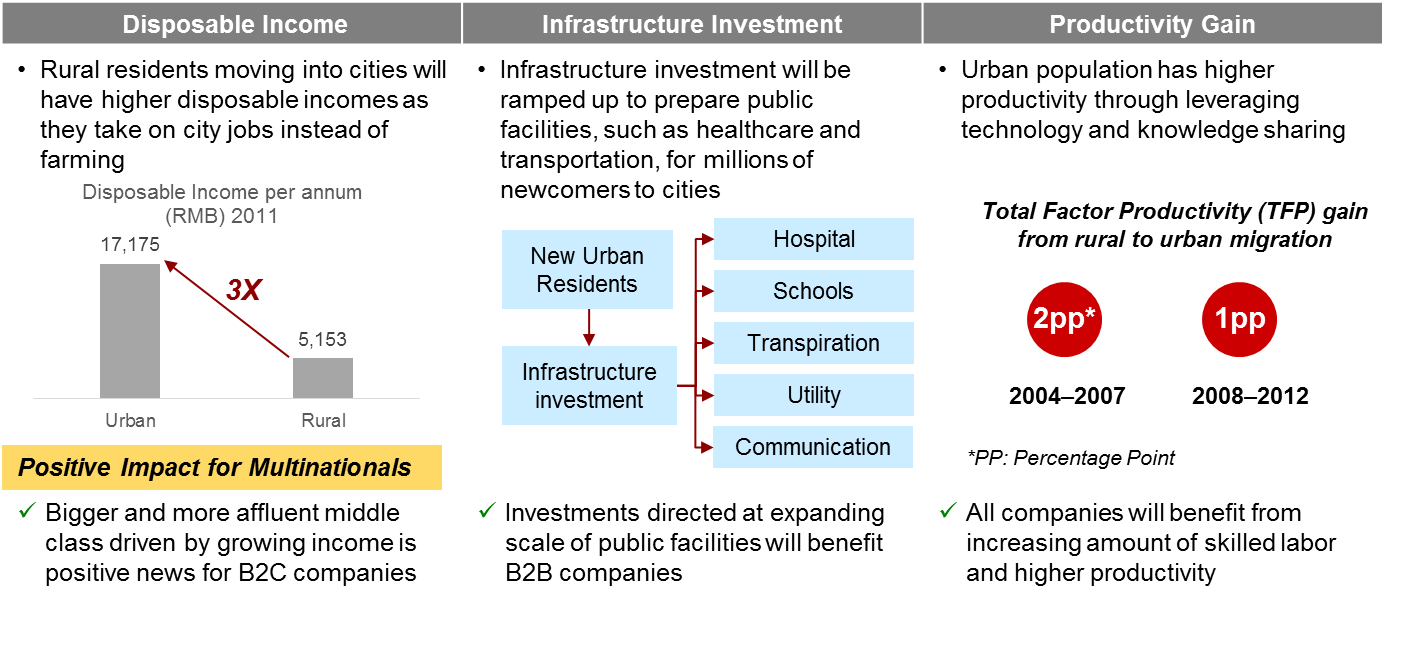

LinkedInContinuing the topic of Provincial Opportunities in China, urbanization will become a major growth driver for China as 250 million farmers will enter cites in coming decade. However, the trajectory of this—the largest urbanization program in human history—is not certain; policymakers and academics are still debating the pros and cons of different urbanization scenarios. The path China eventually takes will have a huge impact on its economic future and wealth distribution, creating both threats and opportunities for multinationals. China’s urbanization plan will create growth opportunities for companies targeting private consumption, infrastructure investment, and productivity gain (see info-graph below)

Provincial governments in China have great power in designing industry polices and approving investment projects. 95% of FDI projects were approved by provincial governments and only 5% by the central government. Therefore, it is critical for multinationals to understand the government’s policy orientation at a provincial level and identify attractive provinces in each industry based on investment level and incentive structure.

Provincial governments in China have great power in designing industry polices and approving investment projects. 95% of FDI projects were approved by provincial governments and only 5% by the central government. Therefore, it is critical for multinationals to understand the government’s policy orientation at a provincial level and identify attractive provinces in each industry based on investment level and incentive structure.

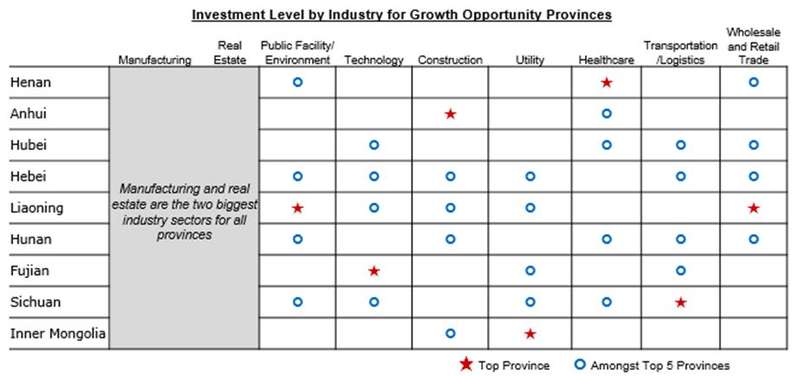

FSG has analyzed the growth opportunity provinces’ competitiveness in nine key industries. Manufacturing and real estate are not ranked, because all provinces invest heavily in those two, which represent about 60% of total investment in aggregate. Other 7 provinces are ranked based on investment level in that particular industry - you may click the image below to enlarge the chart:

")

{kind=link}