LinkedIn

LinkedIn The Fed will delay the tapering of its bond buying program in response to the US government shutdown. For emerging markets this means a slower pace of currency depreciation into year-end, and the potential for limited short-term appreciation in markets that may have over-corrected, like Turkey and Indonesia. With currency depreciation slowing, fourth quarter GDP results may surprise slightly to the upside. The dollar-denominated ETFs that track local Turkish and Indonesian stock markets both increased 4% on the news.

The Fed will delay the tapering of its bond buying program in response to the US government shutdown. For emerging markets this means a slower pace of currency depreciation into year-end, and the potential for limited short-term appreciation in markets that may have over-corrected, like Turkey and Indonesia. With currency depreciation slowing, fourth quarter GDP results may surprise slightly to the upside. The dollar-denominated ETFs that track local Turkish and Indonesian stock markets both increased 4% on the news.

October 2, 2013 By Leave a Comment

What the US Government Shutdown Means For Emerging Markets

September 16, 2013 By Leave a Comment

Emerging Markets Opportunity Not Over

Recent reversals in capital flows caused large and sudden currency devaluations, faster than many emerging markets expected or could manage. As a result, many market commentators have called this end of the emerging markets opportunity. That statement couldn’t be further from the truth. While companies should always expect challenges in emerging markets, the changing environment will also create a new set of opportunities.

Recent reversals in capital flows caused large and sudden currency devaluations, faster than many emerging markets expected or could manage. As a result, many market commentators have called this end of the emerging markets opportunity. That statement couldn’t be further from the truth. While companies should always expect challenges in emerging markets, the changing environment will also create a new set of opportunities.

FSG identified four ways companies can capture growth in this shifting environment:

- Leverage home-currency strength to win share back from emerging markets–based competition

- Double down on local production to reduce production costs

- Use balance sheet strength to earn financing margins

- Reassess customer segmentation to identify local customer “winners”

FSG looks at these strategies and the drivers of the changing global environment in our 2014 Global Performance Drivers report, now available for FSG clients.

What happened?

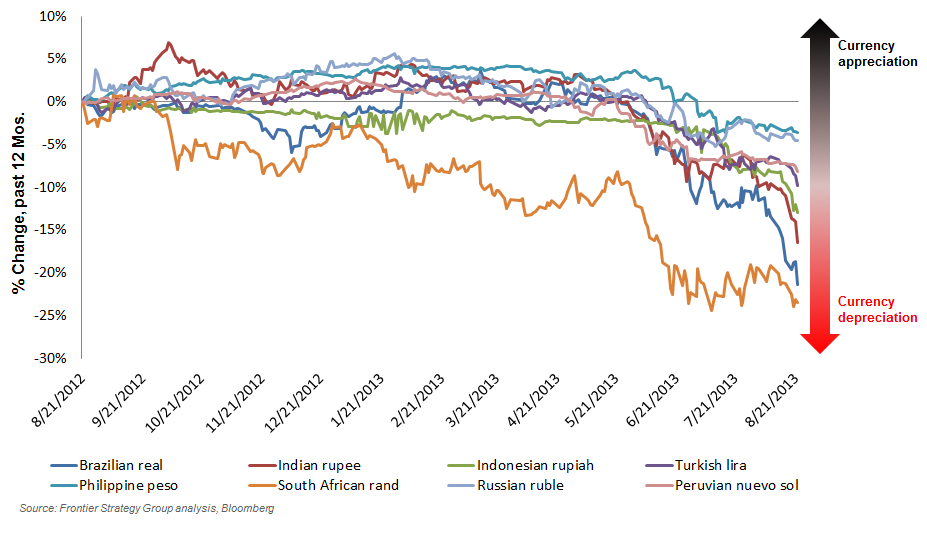

Capital flows reversed because of push and pull factors. As the US economy continues to improve, the Federal Reserve is expected to reduce bond purchases, changing the risk-return payoff for portfolio investors, “pulling” capital out of emerging markets. We also see slowing growth in emerging markets “pushing” capital to developed markets. The outflow of capital is more concerning for countries like Turkey, Poland, and Ukraine, which have high levels of short-term external debt. Countries fitting this profile may run into short-term funding challenges that could drive up local interest rates, or in the worst case cause temporary liquidity problems. Other countries like India and Indonesia may now struggle with inflation as currencies decrease faster than is manageable, driving up costs for consumers.

April 29, 2013 By Leave a Comment

Paying for Flexibility: An Expert’s Take on Mitigating Currency Volatility

U.S.-based multinational corporations lost an estimated $50 billion as a result of currency volatility in 2012. As I referenced in my previous post, FSG projects currency volatility to increase in 2013. No longer can executives only rely on corporate treasury to manage these risks as the potential impacts on profitability and performance are too great.

To better understand some of the operational strategies that executives can use to reduce currency risks, FSG turned to one of our expert advisors, Professor Gordon Bodnar:

- GB: “I encourage companies to think about structuring their operations as much as possible to have flexibility to respond to unexpected currency movement. If currency moves in our favor, can you take advantage of not just increasing dollar price and dollar revenue stream by providing additional service? Same thing for operations on the downside, how are operations structured so that over the short-term you can make adjustments to the pricing or costs structure such that you see a devalued currency by 10% your costs rise by less than 10%”

- GB: “In markets with high volatility, the goal is an options type payoff. Companies often don’t want to do this, as anytime you are creating an option there is an upfront cost. However, the point is that the payment of the premium is necessary to get the payoffs you want…you have the ability to absorb and move across the profitability curve, leading to a higher expected payout”

Larger initial local investments give executives the flexibility to respond to FX volatility with operational rather than financial strategies.

This is obviously a more risky strategy, and Professor Bodnar was kind enough to share a wide array of less risky strategies that I’ll cover in future posts.

___________________________________________________________________________________________

Gordon Bodnar is the Morris W. Offit Professor of International Finance and Director of the International Economics program at The Paul H. Nitze School of Advanced International Studies. He is presently a research associate of the Weiss Center for International Finance and also teaches in the Wharton Executive MBA program at the Wharton School at the University of Pennsylvania. Dr. Bodnar is also the associate editor of European Financial Management, Journal of Asian Economics, and Journal of International Financial Markets, Institutions and Money. He has held appointments as a Research Fellow at the National Bureau of Economic Research and the IMF. He received his Ph.D. in Economics from Princeton University.

As an FSG Expert Advisor, Professor Bodnar is available to FSG clients for consultation on many business issues with key areas of expertise including corporate and risk management. Please contact your account manager for further information or contact us at sales@frontierstrategygroup.com.

April 11, 2013 By Leave a Comment

Emerging Market Currency Volatility…It’s Getting “Real”

“Currencies should not be used as a tool of competitive devaluation. The world should not make the mistake that it has made in the past of using currencies as the tools of economic warfare.”

- George Osborne, Britain’s Finance minister

For emerging market finance ministers, the concept and impact of “currency wars” is very real. As loose monetary policies in developed economies encourage high capital inflows to emerging markets (often referred to as “hot money”), emerging countries struggle to control inflation and the upward pressure on their currencies. This often leads to a surge in competitive devaluations as governments feel compelled to intervene in order to protect fragile domestic economic recoveries, which has the resulting consequence of amplifying currency volatility. However, these competitive devaluations should not be considered as “economic warfare”, they are economic stabilization measures and a natural result of expansionary monetary policy. As many media outlets implicitly (or probably explicitly) understand, conflict is much more exciting than accord. By emphasizing the antagonistic aspects of these decisions, they are unfortunately misleading the public into thinking that these interventions are purely for competitive purposes.

However, multinationals are impacted when emerging markets governments respond to capital inflows by more aggressively printing money to sell on the open market to buy hard currencies. The reality is that the selling of local currency to buy developed-market bonds creates a cycle that further depresses yields in developed markets, pushing more capital to emerging markets, restarting the cycle of currency volatility again. Unfortunately for international executives, currency volatility creates many problems, such as difficulties in:

1. Pricing products

2. Anticipating costs

3. Uncertain business planning

4. Greater reluctance to hire new employees

5. Price instability in commodity markets

For international executives that are increasingly focused on profitability, currency volatility is one of the most important trends to watch this year. For example, a 10% increase in profitability in a given market will be essentially wiped out by a 10% decrease in the value of the local currency when results are reported.

January 17, 2013 By Leave a Comment

Austerity, The “Death Tax”, And How US Debt Ceiling Negotiators Could Learn From Europe

")

The United States media has an interesting relationship with the word “austerity”. Apparently for the US media, austerity measures are a hot-topic in Europe. US publications such as The Wall Street Journal and New York Times have published articles analyzing the austerity measures implemented in regard to budgetary issues in the PIIGS (Portugal, Ireland, Italy, Germany and Spain). Economists from Paul Krugman to Mario Draghi have debated the effectiveness and scope of austerity measures in the processes of fiscal reconsolidation and deficit-cutting. The most recent IMF World Economic Outlook also offers a more quantitative econometric approach on assessing the effects of fiscal consolidation (their opinion was that estimated fiscal multipliers have been systemically too low, essentially saying that the negative short-term effects of fiscal cutbacks have been larger than expected).

Sentiment from FSG executives continues to reaffirm this growing aversion to the word “austerity”, and what it implies. Cost-cutting as the primary strategy for balancing budgets discounts the obvious economic advantages of pursuing a more equalized approach. In some emerging markets that exhibit tremendous growth potential, regional executives are worried that corporate budget-tightening and a laser-like emphasis on profitability is yielding the same short-term negative multiplier effect that the Eurozone just experienced. Harsh austerity to budgets is leaving regional executives with little room for flexibility, and with top-line revenue growth readily available, emerging markets could easily reap huge rewards for executives that are determined to not implement standardized austerity across the board. While spending clearly needs to be reined in, a bit of leeway should be extended in emerging markets where this “multiplier” could provide the biggest benefit to the company as a whole.

Along similar lines, Ernst and Young published a report estimating that banks will need to write down another $175 billion, as bad loans are forecasted to increase to 7.6% in 2013 from 6.8% in 2012. In FSG’s view, the austerity cycle creates deeper recession, weakening the banks further, and propagating this vicious cycle.

However, multinational corporations are not the only entity failing to grasp the insight here. The US Democratic Party is missing a big opportunity to leverage these recent developments in their favor. Many citizens remember the proliferation and media scrutiny of the so-called “Death Tax” before the 2008 general elections, made famous by Frank Luntz. The seemingly innocuous estate (or inheritance in UK) tax was successfully morphed into a diabolical government plot by Republican political strategists. Instead of an accepted status-quo, the estate-tax was used as a political rallying cry. As if this strategy needed further validation, Luntz’s best-selling book is actually titled, “Words That Work: It’s Not What You Say, It’s What People Hear”.

In the United States media, debt-ceiling negotiations have rarely been covered at their most fundamental level, which is the question of “Austerity or Stimulus?” As I have just covered, the word austerity and negative connotations associated with it are capable of triggering powerful images in the mind of the public (Greek protests and rioting anyone?). If democratic strategists begin to pivot their tactics to emphasize the ramifications of austerity, as opposed to spending their time defending the benefits of entitlement programs, then maybe, just maybe…we won’t end up like Greece after all.

December 13, 2012 By Leave a Comment

PODCAST: Three Risks Emerging Markets Face in 2013

In this podcast, FSG senior analyst Sam Osborn highlights the top three global risks executives should be developing contingency plans for. These seemingly local events would have significant ripple effects across emerging markets globally: the US fiscal cliff, the eurozone crisis, and a potential conflict involving Iran. Sam shares key signposts to monitor and implications for MNCs.

To listen to or download the podcast, click on this link to access the iTunes store.

December 6, 2012 By Leave a Comment

3 Reasons Why Emerging Market Executives Need To Contingency Plan Now

Global uncertainty is increasing. The back-and-forth negotiations surrounding policy decisions on the US Fiscal Cliff, Eurozone crisis, and potential conflicts in the Middle East may be intriguing for political scientists, but for global business executives, they are cause for major headache. These policy decisions don’t just affect the upcoming elections; the anemic growth of the global economy is at stake. Any escalation of one of these major drivers of global risk could seriously thwart hard-earned recovery, and plunge the globe into another recession.

With that said, emerging markets continue to show promise for 2013, even in the face of increased global risk. By focusing on economies that are better positioned to withstand the major influencers of uncertainty, and mitigating exposure to economies that are highly susceptible, growth can still be achieved. For example, economies in: Asia Pacific, Sub-Saharan Africa, and parts of Latin America are relatively well insulated. In the near-term, countries such as: Indonesia, Nigeria, Philippines, and Colombia exhibit the necessary growth fundamentals to withstand some of these potential negative shocks. However, looking at the growth fundamentals alone is not enough. Let’s take a closer look at the three big reasons why emerging market executives need to prepare contingency plan as soon as possible.

1. US Fiscal Cliff – How will you plan for a sharp decline in global demand?

The primary determinant of exposure to the US Fiscal cliff is the amount of exports emerging market regions send to the US. However, the ripple-through effects of the US falling over the fiscal cliff (or probably more appropriately, sliding down the fiscal slope) are much more far-reaching. A reduction in US demand will reduce manufacturing as export-led economies rebalance to reach new market equilibriums. This decline in manufacturing will also reduce demand for the input-commodities, adding downward pressure onto commodity prices. Executives that are caught off-guard by the susceptibility of some economies in their portfolio will find themselves playing catch-up in attempting to rebalance their resource allocation.

2. Eurozone Crisis – Are you prepared for a sudden reversal of foreign direct investment flows?

Trade and financial linkages are the fundamental transmission channels of an intensified Eurozone Crisis. A weakening Eurozone economy, combined with heightened perceptions of global risk, could undermine the foreign direct investment inflows that are currently expected to moderately increase for emerging market economies in 2013. Economies that are dependent on advanced economy capital flows for growth could see a major source of investment dry up.

3. Conflict in Middle East – What happens if there is a major oil shock?

Any conflict in the Middle East could result in a major decline in global oil supply, prompting a spike in oil prices. Higher oil prices would reduce sluggish growth and raise production costs (eroding profitability), while upward pressure on inflation could trigger a reassessment of credit supply in emerging markets. All of these factors combined could cripple indebted economies and threaten a liquidity crisis. The susceptibility and flexibility emerging markets have in dealing with this scenario depends on their adequacy of reserves, and their potential to shift production to exports to enhance their repayment capacity. For example, countries such as Ukraine and Poland are in major danger of a liquidity crisis if economic tensions rise due a reduction in global oil supply.

Only by fully understanding the implications and impacts of these events on business can companies appropriately react to the downside possibility. Executives that plan for the worst will find themselves a step-ahead of the competition if any of these risks materialize. In a highly competitive environment, that extra advantage can be the difference between exceeding and missing performance targets.

November 13, 2012 By 2 Comments

Emerging Markets Are Clouded By Increasing Global Uncertainty

Uncertainty in the global economy, primarily a result of questions surrounding policy decisions in the Eurozone and United States as well as the potential for conflict in Iran, is affecting global economic growth prospects. Growth projections for 2013 continue to fall as worries over fiscal consolidation, financial weakness, and high levels of public indebtedness in advanced economies put downward pressure on global growth. In emerging markets, activity has been slowed by weaker demand from advanced economies, policy tightening in response to capacity constraints, and country specific factors. However, emerging markets are now better positioned to be resilient in the face of crisis compared with 2008, due to policy improvements in the fiscal and monetary space.

As financial markets continue to react to the re-election of Barack Obama, emerging markets globally have a keen eye on the developments surrounding the upcoming US Fiscal Cliff. The impacts of automatic spending cuts and tax increases would be seen worldwide, as declining US demand would affect export-dependent economies across the globe. Lower aggregate demand would also yield downward pressure on commodity prices as global manufacturing decelerates, further damaging economies that are dependent on commodity exports. FSG predicts that emerging market oil exporters could witness drastic reductions in real GDP growth, as much as a .8% decline in 2013.

Even with all of the uncertainty in the global economy, FSG has identified a number of emerging markets countries that nonetheless are expected to exhibit strong growth in 2013. These markets tend to fall into one or more of the following buckets:

Improved political stability

- E.g. Vietnam, Thailand

Ample fiscal cushion

- E.g. Angola, Qatar

Relatively insulated from the Eurozone

- E.g. Philippines, Malaysia

Large domestic populations with a booming middle class

- E.g. China, India, Indonesia

In my next post, I’ll discuss some of the implications of the Eurozone debt crisis and a potential conflict involving Iran on emerging markets growth prospects for 2013.

September 25, 2012 By Leave a Comment

Strategic Planning: Enfranchising Your Local Managers

")

I would venture a guess that it’s not exactly common for multinational executives to make an analogy between their local managers and schoolyard recess. Clearly one group is comprised of precocious adults, while the other group, well, is not. However in the strategic planning process, Frontier Strategy Group has identified a surprising amount of similarities in behavior. Often times when local managers engage in the planning process, they are tempted to act as what we have playfully called either victims or bullies.

The “victims” play defense, focusing on keeping expectations on the low end so they can make sure to meet or exceed them. This can manifest in managers consistently providing overly pessimistic forecasts, and constantly communicating upwards regarding current and anticipated market constraints.

The “bullies,” on the other hand, tend to be concerned with expanding their own little fiefdoms, regardless of whether that is the right answer for the organization as a whole. “Bullies,” tend to show up a little less frequently than “victims,” but they may still be a concern in certain pockets of your organization. Bullies are found arguing for expanded operating budgets and are often overly optimistic regardless of whether targets are met in the short-term.

What you want, of course, is for each of your key team leaders to be in a healthy place in the middle of this pendulum. You want them to serve as trusted partners in the planning process with the freedom to speak their minds, the energy to propose some creative and courageous proposals, and the best interests of the health of your overall organization as their guiding concern while planning.

To achieve that end, Frontier Strategy Group has identified a number of strategies that are built on the foundation of:

1. Capturing the wisdom on the front lines

2. Ensuring plan morale stays high

One unique strategy for ensuring that plan morale stays high is the result of an insight that many companies overlook – employees can simultaneously be highly engaged, demonstrating high enthusiasm, and yet be poorly aligned to the strategic direction is trying to work towards. In this case, one Frontier Strategy Group client refers to these types of employees as “Loose Cannons”. Loose Cannons are people you really want to keep in your organization, but they need to be reoriented so that their energy and ability is helpful than potentially damaging or just wasted.

In my next post, we’ll discuss more about how companies are equipping their team leaders to spot and correct Loose Cannons, as well as other strategies for improving overall local team buy-in to the strategic plan.

September 20, 2012 By Leave a Comment

3 Key Objectives of Chinese Government Healthcare Spending

")

In the latest installment of China’s 5-year plan, the government laid out a series of initiatives that will make China one of the largest pharmaceutical markets in the world. China’s pharmaceutical market is expected to grow from $46 billion in 2009 to $178 billion in 2019, and this massive growth is largely being driven by the ongoing healthcare reforms.

These government initiatives are creating massive opportunities for companies with their fingers on the pulse of these programs. Here are three key government objectives and the impacts they are having on our clients:

1) Key Objective – To Provide Universal Healthcare Insurance

Under the healthcare reform, the government introduced two new basic healthcare insurance schemes, NRCMS and BMIUR, to expand coverage among the rural and the poor urban population, respectively. In addition to a much larger population with access to health insurance, reimbursement rates have also increased; which is likely the cause of higher per capita spending on medical examination and treatment in hospitals countrywide.

2) Key Objective – To Improve Healthcare Services at Grassroots Level

As of February 2012, around 2,200 county hospitals and 33,000 primary healthcare institutions have been renovated as part of the healthcare reform, with approximately 70% of township hospitals and 85% of community health centers having been upgraded. In 2010, 627 new hospitals were set up in China, and because of improved spending on healthcare facilities, about 70% of counties have at least one hospital at the secondary level-A. With all of this new construction, there has been a sharp uptick in utilization and demand for diagnostics and examinations.

3) Key Objective – Public Hospital Reform

Introduction of reforms in the public hospital system has been the toughest challenge for the Chinese government; the government’s reform plan includes separation of ownership and management and a gradual elimination of drug margins. This has led to the government announcing policies that promote private sector investment in hospitals. Specifically, the tendering process is now much more in the hands of individual hospitals and lower-tier clinical facilities, which could be a boon for healthcare companies that are able to leverage their geographic reach and local knowledge into a competitive edge during this process.