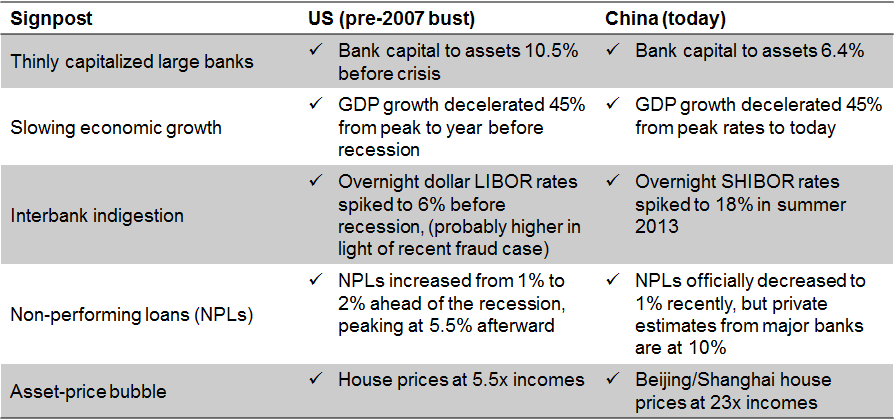

China is the world’s second-largest economy yet many executives ignore it as a source of systemic risk to their global business. The biggest risk in China surrounds its banks, yet we hear little about the problem. Executives in China are often say that the government will simply bail out the system if there were a problem, but that discounts domestic political constraints as well as economic ones. For example, if the Fed, which can print the world’s reserve currency, could barely contain the US banking crisis, what makes us think that China can? Is this time different?

A major shock to the Chinese economy would have a ripple-effect across the globe because of China’s massive demand for commodities and deep trade linkages with Western markets. When China sneezes, the world catches a cold.

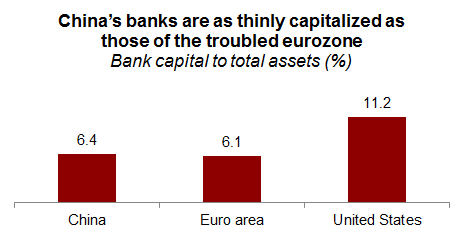

JPMorgan estimates that loans originated by China’s shadow banks may comprise 69% of GDP. With small Chinese businesses unable to secure bank loans, the shadow banking system has flourished. Because of low official deposit rates and restrictions on putting money overseas, savers turn to the shadow banking market to earn higher yields, funding the risky credit cycle, while China’s large banks provide additional leverage via wholesale funding.

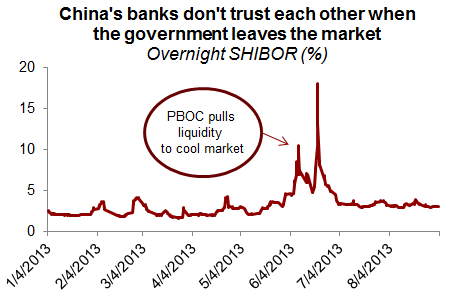

The real risk is not that shadow banks go bad; in fact the Chinese government is actively trying to curb the industry’s growth. Instead the risk is that bad loans in the shadow system bubble up to the systemically important banks that provided wholesale funding, dramatically slowing China’s growth. Officially, non-performing loans are only 1% of total bank loans, but credible private estimates put the number closer to 10% The problem became clear this June when the People’s Bank of China (PBOC, China’s Central Bank) engineered a cash-squeeze to pressure the shadow banks, and the banks stopped lending to each other pushing interbank rates to 13.4% overnight (SHIBOR).

Before the 2007-2008 crises in Europe and the United States, similar interbank indigestion was a strong leading indicator of the looming credit bust.

While the Chinese government is taking actions to manage this risk, companies should also take action by building scenario plans into their long-range business plans. Better to build in insurance, even for something perceived as low risk, as economic history has a tendency to repeat itself.