The case for Brazil is getting harder to make

While the Brazilian economy grew faster than expected during the second quarter, full-fledged recovery remains elusive and several rounds of interest rate hikes have yet to rein in stubbornly high inflation. FSG is expecting relatively weak GDP growth of 2-2.2% YOY in 2013, with potential for electorally-motivated fiscal stimulus to drive growth of around 2.7% YOY in 2014. These numbers are disappointing, and underscore the extent to which Brazil’s long-term potential remains constrained by structural bottlenecks and protectionist policies.

Most multinationals are in Brazil for the long haul, but many plan to limit investment

Here at FSG, we have been carefully tracking multinational sentiment with respect to Brazil, and on a recent trip to Miami, I had the opportunity to sit down with many of the LATAM executives we work with to discuss how the role of Brazil within their regional portfolios has changed as economic growth has slowed.

Suffice it to say that while weak prospects have put a damper on sentiment, few executives are contemplating pulling out of the market. However, many executives I have spoken with in recent weeks anticipate holding investment flat over the near- to medium-term, with the potential for scaling back presence if the situation does not improve over the course of 2014-2015.

Interestingly, this sort of pessimism is gaining ground in spite of high top-line growth. Most executives we work with don’t anticipate that Brazil’s slowdown will have a significant impact on their ability to reach ambitious revenue-growth targets, largely because in a market the size of Brazil, there is still white space to be found. Rather, they are concerned about hitting bottom-line targets, and with good reason: Brazil’s high-cost, protectionist operating environment poses a significant drag on margins for foreign multinationals.

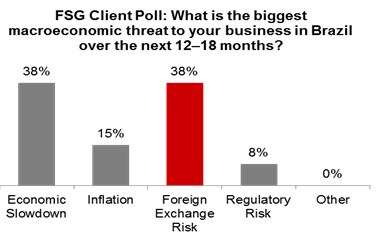

Recent exchange rate volatility is making an already-difficult situation worse

The Brazilian real has been remarkably volatile over the course of Q3-early Q4, depreciating to a low of 2.45 BRL/USD in late August as investors were originally anticipating that the United States would begin to taper bond purchases in September. A majority of companies we work with report that they have built their budgets for 2013 around an anticipated exchange rate of exchange rate of 2.1–2.2 BRL/USD. As such, recent volatility has exacerbated their exposure to FX-related losses and made deal making a herculean endeavor.

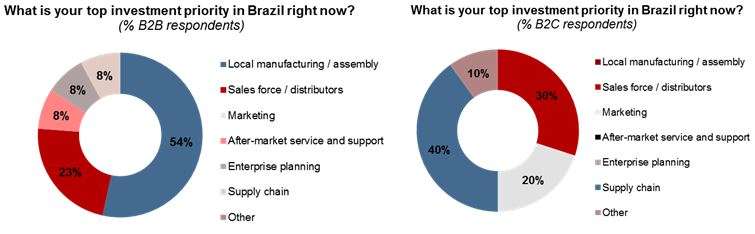

Companies able to take the long view are targeting their investments to improve efficiency

When all is said and done, there is little reason to believe that the protectionist bias of Brazilian labor, tax, and investment policies will change over the medium term. President Rousseff is likely to be re-elected, and domestic politics preclude any marked departure from the ad hoc interventionism that has defined her first term thus far. Executives that are able to plan for the long-term are increasingly coming to terms with this reality and targeting their investments accordingly in an effort to boost profitability. In the B2B space, many companies we work with view investing in local manufacturing as the best way to bring down costs over the medium to long run, while B2C companies are investing in their supply chains.