Podcast: Play in new window | Download

Struggling to Combat Slowing Growth and Rising Costs in Key BRICS Markets?

A conversation with your regional counterpart in EMEA, LATAM, or APAC can help you understand the common structural factors driving lackluster growth and help you re-set corporate expectations for growth in 2014

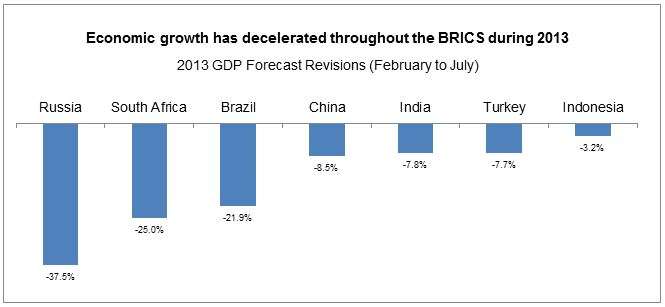

2013 has been a difficult year for the BRICs—economic growth has decelerated across the board due to the confluence of external headwinds and domestic inefficiencies, while the political will to push for necessary structural reforms has proven elusive.

For emerging markets executives seeking to respond to slowing growth in key BRICS markets, cross-regional conversations can be valuable for issue diagnosis and strategy development. The premise of the argument here is a simple one: common problems can and ought to be identified, so that viable strategies for driving profitable growth given less favorable medium-term prospects for the BRICs can be replicated and applied across regions.

I’ve been ruminating about Brazil’s slowdown and potential for recuperation in 2014 for several quarters now, while my EMEA colleague, Martina Bozadzhieva, has been doing the same with respect to Russia. However, it wasn’t until we had an opportunity to sit down together and discuss the dynamics driving Brazil and Russia that we learned how much these two seemingly disparate markets have in common.

Listen to our podcast below for a quick recap of the structural factors driving lackluster growth in Brazil and Russia, and get a cross-regional perspective on strategies for managing corporate expectations and improving bottom-line performance across the BRICS.

Download the podcast or access the entire FSG iTunes library here.