LinkedIn

LinkedIn Germany is at a turning point – or several – as voters go to the polls for the country’s federal legislative elections on September 22. Whether it is yet comfortable with the title, Germany drives the eurozone, and eurozone economic health is the top-down driver of the broader EMEA portfolio.

Germany is at a turning point – or several – as voters go to the polls for the country’s federal legislative elections on September 22. Whether it is yet comfortable with the title, Germany drives the eurozone, and eurozone economic health is the top-down driver of the broader EMEA portfolio.

Meanwhile, Germany is being asked to lead Europe to recovery, but its banks are weak and its export-driven economy is struggling to find customers within the eurozone. Intense debate surrounds the issues of Germany’s economic strength relative to and necessary leadership role in the eurozone, but there has been little discussion of Germany’s fortitude relative to a standard that truly could boost eurozone recovery and re-open opportunities for multinationals in the region. Companies should thus be prepared for the volatility that will shake Germany and ripple into the eurozone and emerging markets in the wake of its national elections.

Expect eurozone volatility to increase after German elections

Chancellor Angela Merkel is expected to keep her post after Germany’s federal legislative elections on September 22. Leaders throughout the eurozone have stalled any meaningful reform as they await any signal of softening in German-led austerity policy toward the eurozone. Such hopes are misplaced and will increase volatility after the election as struggling southern European democracies begin to vote against the austerity policies that are holding their economies down. Although there are expectations for eurozone recovery next year, FSG expects the status quo.

The eurozone’s stagnant economic growth is driving Germany to find new customers

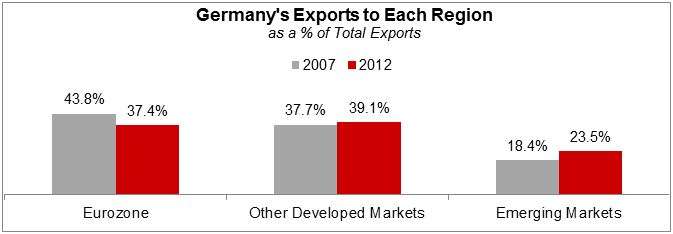

Although the eurozone is still Germany’s largest trading partner, its links to the US and BRICs are larger than what gross trade statistics suggest. FSG is seeing continued eurozone decay drive Germany to export less to the eurozone and more to emerging markets.

However, its reliance on external markets also leaves it vulnerable to external shocks. A simultaneous eurozone squeeze and slowdown of emerging markets will result in a decline in Germany’s ability to prop up eurozone growth.

Germany’s banks remain highly exposed to risk relative to their peers

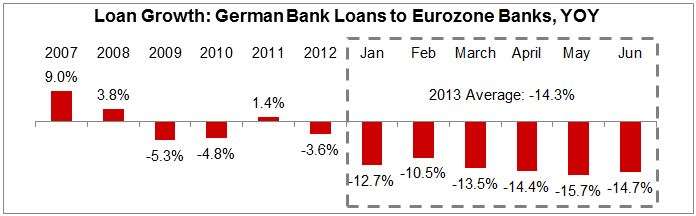

While Germany’s government enjoys “safe haven” status, its banks do not. German banks dramatically slowed lending to each other, with interbank lending decreasing 17.9% YOY in June, due to thin capital ratios, legacy exposure to bad debts yet to be written down, and weak earnings that are not replenishing capital bases.

The German banks’ decline in lending to eurozone by 14.3% YOY in H1 2013 signals that the vicious cycle of credit contraction that began in 2007 will continue to limit growth in Germany and across the eurozone. As banks slow lending to one another in Germany and across the eurozone, credit creation will stall as well.

Despite its challenges, the eurozone still represents US$9 trillion in consumer spending per year, bigger than APAC and CEE combined. FSG is thus monitoring these trends in order to help clients to anticipate ways to increase margin share in the stagnant eurozone economic environment, and to get ahead of any recovery.

FSG clients may read further in our recently released report: Quarterly Market Review: Germany Q3 3013.