If you are a Chinese reader focused on growth in emerging markets, Frontier Strategy Group‘s column “Overseas Strategy” in Fortune China is an excellent source for the latest best practices companies are implementing to fuel their growth. Overseas Strategy is a bi-weekly column in Fortune China and can be found by clicking on this link.

If you are a Chinese reader focused on growth in emerging markets, Frontier Strategy Group‘s column “Overseas Strategy” in Fortune China is an excellent source for the latest best practices companies are implementing to fuel their growth. Overseas Strategy is a bi-weekly column in Fortune China and can be found by clicking on this link.

Featured Emerging Markets Insights

WEBINAR: Winning the Battle for the Emerging Market Consumer

How can consumer companies capitalize on the growth opportunity in emerging markets? Retail and consumer goods executives are turning their attention to the roughly 3 billion shoppers in emerging markets - who will account for 75% of global growth in consumer expenditure through 2015.

Brazilian Trade Disputes Challenging Latin America-Focused Executives

Frontier Strategy Group’s Latin American clients are reporting lost opportunities and revenue due to increasing trade restrictions on imports into Brazil. Costs and frustrations are mounting for businesses dependent upon a smooth flow of commerce across Brazil’s borders, forcing a reconsideration of previous business models due to critical vulnerabilities to import restriction.

MENA Instability is a Wake-Up Call for Companies to Engage Governments

FSG Expert Adviser, Judith Barnett explains why now is the time for multinational companies to engage governments in the Middle East

Africa’s broadening horizons - Financial Times Feature

Africa's Broadening Horizons: Frontier Strategy Group - Financial Times feature on African investment opportunities for multinational companies

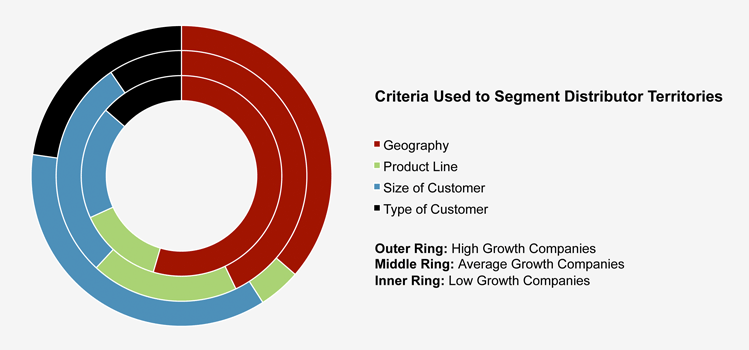

Optimizing Distributor Segmentation in Emerging Markets

How are leading companies segmenting their distributors and assigning territories? Frontier Strategy Group’s Director of Strategic Research, Chris Moore, shares best practices from leading Fortune 500 multinational firms operating in emerging markets.

The criteria MNCs use to evaluate their distributors are designed to maximize the speed and breadth of initial market penetration, but over the long term incentive distributors to seek short-term gain rather than support their foreign partner in establishing a strong market presence.

Implications for MNCs:

- As a result of this evaluation process, most MNCs have developed distributor relationships that are optimal in the early stages of market entry, but over time become less useful

- However, many companies fail to upgrade and restructure these relationship to position themselves for long-term growth.

The three most critical considerations when deciding to relocate manufacturing are:

- Total manufacturing cost (as opposed to labor cost)

- Markets to serve: Domestic vs. Exports to developed markets

- Capital intensity: Labor intensive vs. Capital intensive

Click here to listen to the full Podcast:

Audio clip: Adobe Flash Player (version 9 or above) is required to play this audio clip. Download the latest version here. You also need to have JavaScript enabled in your browser.

The Asia Pacific region is one of the most diverse territories to conduct business in. For senior executives charged with growing Asian markets, their country portfolio typically extends from as far north as South Korea, to Australia in the far south – covering everything else in between. It’s hard to imagine the challenges CMOs must face as they create their brand for the first time in emerging markets such as China and India, while maintaining their position in developed markets. Frontier Strategy Group’s Associate Vice President, Chris Moore sought out the expertise of Brocade’s Asia Pacific senior management team, winner of the 2011 CMO Asia award for brand excellence in the region. In the following interview, Deb Dutta, Vice President of Asia Pacific and KP Unnikrishnan (Unni), Director of Marketing share their best practices for successfully building the Brocade brand in Asia.

How do you balance between maintaining a consistent global brand versus adapting your message within the local context of Asian markets?

Brocade has been in the Asia Pacific and Japan region for 11 years now. We take pride in the fact that we understood the potential of the region and invested early. From early on we did not just leverage Asia as a place to sell our products, but to also build our products presence. In fact, some of the early brand-building campaigns that we first implemented in Asia were later replicated around the world. One of our key philosophies is that while we have a global strategy, we adapt our approach for the local markets. The CMO award was a great example as we were able to go to our customers in Asia and offer them an opportunity to build their brand on a global scale through a joint advertising campaign published in Forbes. We created a true win-win solution in which our local customers partnered with a global brand in Brocade to establish their own brand in Asia and worldwide.

What are some of the mechanisms that you have in place for keeping abreast of the local market trends and incorporating that feedback into how you position the Brocade brand?

There are quite a few things that we have done to localize our business, but one is definitely the partnership we have with Frontier Strategy Group in terms of really understanding the market and the trends that we need to be aware of in the Asia Pacific region. It is a combination of working with strong advisory groups such as yours, partnering with local industry associations, local media houses, and lastly working with our alliances partners. All of these relationships bring a lot of local flavor into what we are doing because it helps us understand what our customers’ needs are and gives us local visibility for when we run campaigns and demand generation initiatives in these markets.

How much of a role does the sales team play in building the Brocade brand in their territories?

We strongly believe that every employee at Brocade is a brand ambassador. We are aggressively working inside and outside the organization to position them as thought leaders in the industry. We support the sales teams to attend local industry forums and even speak at these types of events. Senior sales leaders are encouraged to engage with the media and support our brand building efforts as well. We actually have media training programs plus social media programs to ensure our employees understand how to best represent the Brocade brand in the marketplace leveraging the latest communication trends and tools. Our customers’ willingness to discuss with the media about their success stories partnering with Brocade is a direct result of our sales organization building strategic relationships with our customers.

How do you think about mitigating or managing the risk of giving third parties (such as distributors) access to your brand?

Our business model is a 100% partner model in Asia. We strongly believe that this is the best way to scale our business given the diversity of the region. We take part in joint marketing initiatives with our partners. We review plans and forecasts with them on a quarterly basis and ensure that the dollars put into our campaigns link back to the plan, which in turn link back to revenue generation. We put a lot of strong discipline and process into it. Our 360 degree approach involves working with marketing agencies, telemarketing to create demand and partners then convert leads into closed business. Each group knows what everyone else is doing because we are all working towards the same goal. Most partners even know what our strategic direction and focuses are so when we collaborate on a joint investment it can be a win-win for both sides. We also set clear standard operating procedures for how we onboard and certify our partners. This is an ongoing exercise though, because there is a lot of attrition that happens in Asia. We need to make sure that all channel partners undergo the same level of training so that all partners are as skilled at representing the Brocade brand as the Brocade team members themselves.

When you think about communicating with your customers or your prospective customers how do you see the channels evolving over time?

We have a program called the Alliance Partner Network which is a portal we developed for all of our channel partners. Through this online portal, a mobile application and quarterly newsletters we ensure customers are always aware of the latest developments happening at Brocade. We have also built portals that are more specific for the local needs of the partners in Asia. For example, if we release new products in the local market, the partner can login and take part in an online training to understand how to best position the product in the marketplace. The partner doesn’t need to invest in his own go-to-market resources; we provide everything in a fully-customizable format through our portal. The portal is a communicative platform that allows us to both provide partners with the tools they need to sell our products, and capture valuable feedback from our customers about the realities of on-the-ground market conditions.

The prospects for emerging markets are looking good, analysts say.

Global markets may have entered a state of panic, with investors paying little regard to fundamentals, according to Jerome Booth, head of research for Ashmore, but valuations of emerging market assets are “sharply at odds with underlying risks,” and there’s considerable value across the emerging market complex.

“EM assets have sold off due to significant growth and fiscal challenges in [Group of 10] economies,” he said in a recent research note. “While these difficulties will take years to play out, we believe the end-game is now in sight for the most serious tail risks in G-10. The current global sell-off is likely to be over in the coming weeks.”

And the outlook for EMs remains positive, with their economies increasingly insulated from G-10 developments because of “solid domestic demand, strong reserve cushions, and domestic financing sources,” Booth said, adding that EMs will continue to grow 3 times as fast as G-10, while carrying less than one-third of the public debt levels of the G-10 economies.

The iShares MSCI Emerging Market Index Fund EEM has already lost more than 28% year to date.

“The emerging markets represent long-term value, and have been mispriced as capital flees to the dollar,” said Matt Lasov, director of global research at Frontier Strategy Group.

And with that comes opportunity.

Multinational corporations are holding record levels of cash and should use this “as an indicator to begin serious conversations for acquisition targets,” said Lasov. “As there are limited high-quality targets in emerging markets, first movers will gain an advantage over competitors in terms of the quality of the assets as well as the valuation.”

The recent headlines out of Mexico paint a seemingly dichotomous picture: violence is at an all-time high, yet multinationals continue to pour money into the country, with over $22 billion in foreign direct investment expected this year. The implication is that the knock-on effect to multinationals from the government’s war on the drug cartels has been slight. However, this interpretation of the facts belies the impact that violence-induced migration is beginning to have on many multinationals in the country. Recently, while in Mexico City, we heard over and over again of the many ways in which violence is changing demographic realities as workers and consumers move away from areas plagued by high levels of cartel activity.

As Calderón’s war against the cartels drags on, violence-induced migration is accelerating, creating a new set of challenges for multinationals. States with the highest levels of violence, such as Chihuahua, Sinaloa, and Guerrero, are seeing a net loss of citizens to more peaceful states like Querétaro and Hidalgo. According to Frontier Strategy Group Expert Advisor Leon Kraig, “many companies are starting to feel the impact of white collar flight from Monterrey” finding themselves unable to find entry- and mid- level managers. “Asking employees with families to move there is very difficult, and many based in Monterrey are asking to be transferred. Companies looking at alternative locations are primarily considering Mexico City, or possibly Guadalajara or Querétaro”, says Kraig.

In addition to tightening the labor market, violence is also changing the behavior of consumer markets. It is estimated that 230,000 people have been displaced in Mexico due to cartel violence, a tragedy that is shifting the demographic composition of many cities. Additionally, consumption patterns are changing as many individuals grow reluctant to frequent public venues such as restaurants and markets that could be targeted by cartels. According to a senior executive of a major global alcohol distiller, “Nobody is going out to bars and restaurants at night, so our business is suffering significantly in Monterrey, because consumers don’t compensate by entertaining more at home.”

One of the major drivers behind the decision of many Mexicans to relocate away from violent areas is the government’s lack of any viable near-term solution for dealing with the cartels. Indeed, violence has steadily increased with each new phase of the government’s war on organized crime, with the number of homicides growing by 15% year-on-year during the first half of 2011 alone. Given that only long-term efforts to strengthen judicial and police institutions are likely to have any major impact on the security situation, an adjustment to the government’s current strategy is unlikely over the near term. Many Mexicans therefore feel unable to wait out the increased violence as they have previously.

As the violence in Mexico continues, multinationals should expect to see skilled labor markets in the northern parts of the country tighten, driving up costs for companies seeking to efficiently manage their manufacturing operations. Additionally, B2C companies must keep an eye on how the violence is affecting demographic trends and consumption patterns. It is our belief that the companies that can adapt their strategies to these changing dynamics will see the least impact from continued violence.

")

Most Asian countries continue to exhibit strong growth despite the recent turmoil in global markets. However, if there is a full-blown recession in the developed world, some markets will weather the storm better than others. In particular, domestically-oriented countries like India and Indonesia will be much less affected by a downturn in the West than will export-oriented countries like Thailand and Malaysia

- Bangladesh: Bangladesh’s deal with India will likely lead to long-term growth of bilateral trade and improvement of domestic infrastructure

- Cambodia: As Cambodia becomes increasingly integrated into the regional and global economies, it will start drawing significant attention from investors

- China: Signs of weakening consumer demand have appeared in the luxury goods industry, which has seen stellar growth numbers in H1 2011

- India: Continuing interest rate hikes along with inflationary pressures will dampen GDP and industrial growth for the remainder of 2011

- Indonesia: MNCs should ensure that they are effectively taking advantage of Indonesia’s numerous government incentive programs

- Japan: The economy’s slow path to recovery will further decelerate due to the global economic slowdown, rising Yen, and continuing energy issues

- Malaysia: Malaysia is pursuing an unprecedented expansion of its oil infrastructure that may create significant opportunities for multinationals

- Pakistan: Companies should expect price pressures in Pakistan to remain elevated for the foreseeable future

- Philippines: A new agreement with China will bolster bilateral trade and boost foreign direct investment in the Philippines

- South Korea: New anti-graft reform measures should help to improve South Korea’s corruption landscape over the medium term

- Taiwan: Taiwan’s business environment will continue to improve as the island’s leaders work proactively to attract investment

- Thailand: Companies should remain cautious of the political landscape until the country’s new government has established a solid base of support

- Vietnam: The government’s new minimum wage hike will undergird Vietnam’s inflationary spiral, prolonging the pain for multinationals in the country

Working with local partners has been a winning strategy for many MNCs interested in the Russian market. However, with increased concerns about FCPA and UK Bribery Act enforcement, MNCs are more than ever seeking to ensure their Russian partners are not engaging in any corrupt practices.

In theory, MNCs can protect themselves by conducting extensive due diligence on any potential partners, including compliance clauses in their contracts with their partners, and carefully monitoring for any suspicious activity.

In practice, however, “Some companies are so eager to enter the market, they rush into partnerships believing everything their Russian counterparts tell them. They allow themselves to be seduced by local partners,” says Tim Stanley, formerly with Control Risks and KPMG and now Frontier Strategy Group expert advisor and independent consultant with extensive experience in conducting integrity and operational due diligence for companies investing in Russia and throughout the CIS.

“There is often a huge gap between how foreign companies expect their local partners to work, and how their Russian counterparts actually operate on the ground. The gap may not become obvious for a while, especially if foreign company representatives only occasionally meet with their Russian partners,” points out Tim Stanley.

He adds that Russian firms may sometimes not share the details of how they get things done with their foreign partners, because they believe all that matters to the foreign company is good financial results. “Communicating to your partners the importance of ensuring compliance in all their actions is key,” says Mr. Stanley. “And doing so not just once, but on a continuous basis.”

Mr. Stanley offers a few other tips for foreign companies working with local partners in Russia:

When evaluating potential partners: know who runs the company, and who actually owns it

Who legally owns the company and who runs it can differ greatly in Russia, and MNCs should see any inconsistencies in the ownership and management structures of potential partners as a red flag. Some Russian companies have immensely complicated ownership structures, sometimes for legitimate reasons but often created with the purpose of tax evasion and other illegal practices. The real owners may present operational, reputational and political risks significantly different from those which an unwitting investor or business partner may be aware of when negotiating with local management.

Reputational due diligence is extremely effective in Russia

Often in Russia, word of mouth can give you a better perspective on a potential partner than a review of their financials. Get a second or third opinion on a potential partner, learn about their reputation and the experiences other companies – especially Western ones – have had working with them. If the company has a local track record of legal disputes, or a reputation for using aggressive business tactics or for cutting corners, then chances are, you will hear about it.

Due diligence does not end with a signed contract

Over time a company’s profile will change as business activities adapt and develop. A company’s compliance profile – and thus potential vulnerability - will change in step with the changing nature of the company, with some risks becoming more prevalent and others diminishing. A clean bill of health during the pre-transaction due diligence is a necessary, but not sufficient condition for compliance purposes, and foreign investors need to invest in promoting a culture of integrity and compliance in their dealings with local companies. This can be achieved by embedding compliance throughout the company’s operational activities, and through regular communication and training.

(5) With a mandate to govern, can Nigeria’s new government implement positive and sustainable reforms?

Between its petroleum-dominated economics and mind-bending demographics, Nigeria is well-positioned for sustained growth and diversified foreign direct investment in the decade ahead: a leading economist has picked the country to be the world’s fastest growing across the four decades to 2050. With its new government now in place for the best part of four years following the 2011 elections cycle - including key individuals favored by business in seat at the both the Finance Ministry and the Central Bank - the time is overdue for a meaningful political vision to capture that opportunity and steer the country towards its eventual destiny as Africa’s regional super-power. Following the creation of a sovereign wealth fund to manage oil-related windfalls and restructuring of the country’s troubled banking sector under the previous administration, future critical reform milestones to look for in President Goodluck Jonathan’s first full term must include tangible progress on tackling entrenched official corruption at all levels of the country’s extensive bureaucracy. In terms of both their immediate creation of investment opportunities and their wider demonstration of an improvement rather than inertia culture in the country’s legislative system, meanwhile, movement will also be expected on finally enacting long-overdue measures to reform the country’s hydrocarbons industry (the delayed Petroleum Industry Bill) and to liberalize the its public healthcare provision (the National Healthcare Bill, now over six years in hiatus).

(6) Will there be a leadership challenge in South Africa?

Better the devil you know, or the devil you don’t? That’s the dilemma facing many businesses with a footprint in South Africa as they contemplate the possibility of controversial President Jacob Zuma facing a serious challenge to his leadership position and broader policy platform at the ruling African National Congress (ANC)’s elective conference in Mangaung (Bloemfontein) in December 2012. Zuma has disappointed businesses with his inability to kick South Africa’s economy into rapid growth, his apparent inertia (and, at times, alleged complicity) in the face of creeping official corruption at all levels of the country’s bureaucracy, and perhaps most damagingly his ambivalence to growing calls from the ANC’s radical youth wing (the ANCYL) for the nationalization of various sectors of the private economy. Ironically, however, it is steps in recent weeks by Zuma’s leadership team belatedly to silence the ANCYL’s outspoken leader Julius Malema – whose support was critical to Zuma’s initial ascendancy - that have upped the stakes for Mangaung and created the possibility of serious attempts throughout 2012 to displace pro-business moderates from government.

(7) Will Asian companies continue to make the running in Africa?

The story of Chinese investment, and to a slightly lesser extent companies that hail from other Asian countries, in Africa is a popular academic and media topic. The appetite for African growth from businesses that honed their model in Asia is apparently boundless. Asian vehicle manufacturers Honda, Hyundai, Toyota, Suzuki, Tata and Mahindra have all set their sights on South Africa; Samsung hopes to generate $10 billion in annual revenue in Africa by 2015 with a R&D hub in Kenya; and in recent weeks Chinese handsets manufacturer Huawei has announced a major play for the booming Nigerian telecommunications market. Part of Africa’s attractiveness as a market – beyond its raw consumer potential – is its relatively uncluttered competitive landscape. With every year that passes, that scenery becomes more congested. Western companies arguably already lag behind their Eastern counterparts in numerous markets across various verticals; the danger is that recession or slowdown in their home markets into 2012 sees Western firms revisit ever stronger conservatism and risk aversion towards the African opportunity, despite its favorable growth profile, allowing that gap to widen further – potentially beyond reach – as Asian investment continues to flow unchecked into the continent. Meanwhile, side-effects of this trend can also be expected to accelerate in 2012: diversifying trade and investment partners strengthens the hands of African governments, and lessens their dependence on, and motivation to defer to the legislative and regulatory preferences of, Western operators. Given many Asian investors’ emphasis on long-term manufacturing, research/development and supporting infrastructure components to their investments, the overall bar for all businesses entering the market can also be elevated as a result; relationships between employees and host communities and investing businesses can also be substantially altered by these Asian pioneers.

(8) Can East Africa meaningfully integrate?

The East African Community regional bloc (comprising Kenya, Tanzania, Uganda, Rwanda and Burundi) on 1 January 2010 formally launched a common market. All five countries have already adopted a common external tariff, an identical tax applied to imports from outside the bloc, and allowed duty-free regional trade with the exception of Kenya, the largest economy. Given that East Africa lacks a single economy of the scale of Nigeria in the west or South Africa in the south, material progress on implementing the common market and transitioning towards the free movement of people, capital and services across the five countries’ borders, as well as the abolition of import duties, is critical to the region’s future growth prospects. If precedent is a guide, implementation during 2012 and beyond is likely to be under-funded and therefore slow and patchy – while structural obstacles to meaningful integration from both inadequate transportation infrastructure and deficient electrical power supplies will remain significant. Nevertheless, with its booming demographics and swelling natural resource potential as well as its proximity to Middle Eastern and other Asian markets, East Africa remains an exciting growth frontier for investment. Ultimately, the aim is also to introduce a single EAC currency to further simplify regional trade.

To learn more about Frontier Strategy Group’s regular Market Intelligence on Africa’s key investment markets, contact africa@frontierstrategygroup.com to learn how we can help

- (Tradition continues along Mozambique’s Maputo Development Corridor)

Part one

With unprecedented levels of investor interest both on merit, and because growth may well prove elusive elsewhere, 2012 promises to be an exciting year for sub-Saharan Africa. In this two-part series, I examine some of the key questions businesses looking to the continent should ask themselves as they plan ahead:

(1) Can the continent withstand continuing volatility in commodity prices?

While broadly insulated from sovereign debt and banking-related contagion from the OECD countries, Africa’s vulnerability to commodity price movements – particularly in the form of inflation – remains considerable, and will be a key theme for the region’s macro-economic outlook alongside an average 5.25-5.75% GDP growth projection into 2012, driven by strong domestic consumption. Importers of food and fuel – including Ethiopia, Kenya and Uganda – are already facing sharp inflationary pressure, a situation that could worsen in the year ahead if costs for those inputs trend upward. Producers of oil and industrial metals – Angola and Nigeria the giants in the former category, countries such as Zambia and Congo (DRC) falling in the latter – will meanwhile see their fortunes rise or fall depending on global commodity price and demand shifts, with higher prices boosting government currency earnings but also creating upward pressure on domestic prices. A renewed recession in Western markets, meanwhile, would impact African economies through lower remittances and renewed risk aversion amongst investors from those affected countries. South Africa, with its exposures on metals prices, established manufacturing exports, developed tourism sector, looks particularly vulnerable should worst-case macro-economic scenarios play out in North America, Western Europe and Japan.

(2) Will a series of major elections cause seismic shifts or entrench the status quo?

2011 has been a busy time for elections in Africa: larger countries that have been or are yet to go to the polls this year include Cameroon, Congo (DRC), Nigeria, Uganda and Zambia. Assuming Zimbabwe’s vote is delayed as expected, that country will join a similarly important list for 2012 that also includes Angola, Ghana, Kenya (whose outlook I cover in more detail elsewhere in this list), Mali and Senegal. In addition to the familiar potential for delays, disputes and protests, this wave of elections could be demonstrative of a number of wider cross-border trends. To begin with, that so many countries are organizing and holding broadly free and fair voting each year represents a dramatic and continuing important shift away from the autocratic norms of the 1980s and early 1990s. On the flip side, with accountability and transparency also comes greater policy unpredictability – as mining companies in Guinea discovered in 2010, when a change of president via the ballot box in that country catalyzed a major review of mining licences and royalty payments. Many of the elections will pit very elderly incumbents – Senegal’s Wade and Zimbabwe’s Mugabe are both over 85, while Angola’s dos Santos is entering his 70s – against younger opponents promising an agenda of change, reform and renewal. In addition to generational and policy change, how to manage and beneficially spend these countries’ growing mineral wealth will be a prominent issue in many of the elections – most especially in oil- and diamond-rich Angola and in Ghana’s first vote since it joined the ranks of petroleum producers, but also in Mali and Zimbabwe where mineral finds have yielded much-needed new government revenue streams.

(3) Will North Africa’s wave of anti-government protests shift southwards?

It hasn’t escaped the notice of many Africa watchers that the same cocktail of raw ingredients that broadly underpinned the so-called Arab Spring – long-entrenched and corrupt undemocratic regimes presiding over increasingly youthful and socially connected, technology-savvy populations struggling with unemployment – are also present in a fair number of sub-Saharan countries. It should be noted that mass uprisings leading to regime change are not unknown in the region – the toppling of Madagascar’s previous president in 2009 providing but one recent example – while military-led coups, although far rarer than in previous decades, also continue to occur sporadically in some countries. For some, the question has become why such ‘revolutions’ are not more commonplace given the potentially volatile causal factors in place. The answer to that question likely varies location, but includes – channeling de Tocqueville’s theory of what causes revolutions – a certain degree of lower expectations on the part of poorer African populations (often focused more on basic subsistence / survival or emigrating than marching on the streets) than their Arab counterparts, combined with governments that by and large have still maintained a sufficient monopoly of force and willingness to stamp out dissent fairly ruthlessly before it spreads. With public expectations rising alongside GDP – and food prices – in the months ahead, the potential for more unrest during 2012 is highly credible. Whether this manifests as more ‘manageable’ street protests of the type witnessed already in a number of countries during 2011 (such as Burkina Faso, Mauritania and Uganda) or more sustained disturbances remains to be seen. Other candidate countries for turmoil in the year ahead include Senegal, Gabon, Zimbabwe and Cameroon.

(4) Can Kenya come through a pivotal year unscathed?

It’s been a tough few weeks for Kenya, East Africa’s critical hub market: from the serious food crisis in its north, through the abduction of a female British tourist and the murder of her husband in the coastal resort of Lamu, to a major pipeline fire near the capital Nairobi. The negative impact of such developments on tourist visitor numbers and investor appetite would be negligible compared to the situation should the serious nationwide political violence that accompanied its December 2007 election resurface surrounding new polls due in August 2012. The implementation of a new constitution and wider Kenyan politics remain effectively on hold pending the long-awaited start of hearings at the International Criminal Court in The Hague, involving a number of key politicians accused of involvement in the clashes that paralyzed the country in 2007-2008. Any resurgence in political violence due to the Court’s findings or around the next poll will reverse recovery in the tourism sector, and with it any chance of growth close to the 5.7% YOY GDP figure projected for 2011. In the long-term Kenyan politics needs to move on from confrontational, ethnic-based divisions into more ideological / policy-based debates in order to achieve stabilization and much-needed reform.

To learn more about Frontier Strategy Group’s regular Market Intelligence on Africa’s key investment markets, contact africa@frontierstrategygroup.com to learn how we can help

Featured Authors

-