Berlusconi’s exit may mark the beginning of the breakup of the European Monetary Union (EMU), changing the business environment in Europe and markets globally. The problem in Italy lies in the country’s politics, not its economics; if the political class demonstrates they will do what is necessary, catastrophe can be averted. And over the past half century, Italy has often done the right thing (usually after exhausting all other options). The country’s politicians turned a ruined country into the world’s 8th largest economy, outwitted the most powerful and genuinely popular communist party in the western world, and entered the Euro, to name just a few accomplishments. Unfortunately, the challenge before them today is far greater and far less conducive to political machinations. The country has to decide whether it will be a competitive and dynamic economy or a larger version of Greece; the health of the world economy, and the future of the Euro, hang on the balance.

Berlusconi’s exit may mark the beginning of the breakup of the European Monetary Union (EMU), changing the business environment in Europe and markets globally. The problem in Italy lies in the country’s politics, not its economics; if the political class demonstrates they will do what is necessary, catastrophe can be averted. And over the past half century, Italy has often done the right thing (usually after exhausting all other options). The country’s politicians turned a ruined country into the world’s 8th largest economy, outwitted the most powerful and genuinely popular communist party in the western world, and entered the Euro, to name just a few accomplishments. Unfortunately, the challenge before them today is far greater and far less conducive to political machinations. The country has to decide whether it will be a competitive and dynamic economy or a larger version of Greece; the health of the world economy, and the future of the Euro, hang on the balance.

Featured Emerging Markets Insights

WEBINAR: Winning the Battle for the Emerging Market Consumer

How can consumer companies capitalize on the growth opportunity in emerging markets? Retail and consumer goods executives are turning their attention to the roughly 3 billion shoppers in emerging markets - who will account for 75% of global growth in consumer expenditure through 2015.

Brazilian Trade Disputes Challenging Latin America-Focused Executives

Frontier Strategy Group’s Latin American clients are reporting lost opportunities and revenue due to increasing trade restrictions on imports into Brazil. Costs and frustrations are mounting for businesses dependent upon a smooth flow of commerce across Brazil’s borders, forcing a reconsideration of previous business models due to critical vulnerabilities to import restriction.

MENA Instability is a Wake-Up Call for Companies to Engage Governments

FSG Expert Adviser, Judith Barnett explains why now is the time for multinational companies to engage governments in the Middle East

Africa’s broadening horizons - Financial Times Feature

Africa's Broadening Horizons: Frontier Strategy Group - Financial Times feature on African investment opportunities for multinational companies

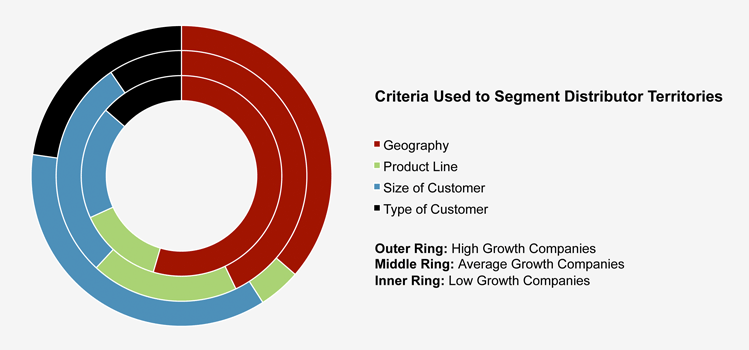

Optimizing Distributor Segmentation in Emerging Markets

How are leading companies segmenting their distributors and assigning territories? Frontier Strategy Group’s Director of Strategic Research, Chris Moore, shares best practices from leading Fortune 500 multinational firms operating in emerging markets.

Frontier Strategy Group appeared in yesterday’s Financial Times in an article titled, Gems: Making the case for Gems

According to the Frontier Strategy Group, while China’s growth may be slowing down, India’s is increasing, and by 2014, India’s growth rate will outstrip China’s, at 8.6 per cent compared with 8.2 per cent. This has prompted fears of a hard landing for China.

For much of the past year, China’s policymakers have been grappling with how to temper sharply rising asset and consumer prices and dampen the ill-effects of an unprecedented economic stimulus following the global financial crisis – without torpedoing strong economic growth.

China first set about reining in credit in April 2010, following a record RMB12.2trn (£1.1trn) surge in bank lending since the start of 2009, according to China Economic Research.

The Frontier Strategy Group predicts that China will have trouble in tackling its public debt and its debt to GDP ration will rise from 16.2 per cent in 2011, to 16.3 per cent in 2012, 2013 and 2014, before going back down to 16.2 per cent in 2015.

German Chancellor Angela Merkel’s party voted today to provide a means for Euro-zone markets to voluntarily exit the Euro without losing access to the EU’s free trade zone. This move confirms that Germany is not willing to save the Euro in its current form and will begin to put in place additional mechanisms that will lead to exits from the Euro.

Retaining free trade with the rest of the continent is the key issue for markets like Greece, Italy, Portugal and Spain who would become more competitive overnight with a devalued currency and access to open borders.

If accepted by the broader EU, the move will make an exit easier for troubled markets, but it may also put undue pressure on the banking systems in Germany and France. Any exit would cause default, meaning that German and French banks have to absorb losses on bad debt and associated derivatives. A preemptive strategy to recapitalize banks will be required if Germany is to protect itself while paving the way for weaker markets to leave the Euro.

The economic environment is full of uncertainties for companies operating in both developed and emerging markets. However, uncertainty can be the best environment for stimulation of long-term growth. To make the best investment decisions in this climate, managers will require reliable, up-to-date data and best practices and must learn from those who have succeeded and failed ahead of them. Companies that move first to pursue growth during this downturn will become the market leaders when the global economy inevitably recovers.

The economic environment is full of uncertainties for companies operating in both developed and emerging markets. However, uncertainty can be the best environment for stimulation of long-term growth. To make the best investment decisions in this climate, managers will require reliable, up-to-date data and best practices and must learn from those who have succeeded and failed ahead of them. Companies that move first to pursue growth during this downturn will become the market leaders when the global economy inevitably recovers.

Prioritizing markets and thoroughly performing due diligence are essential pre-integration procedures that need to be carefully considered. An estimated 50-70% of acquisitions fail to deliver on their expected value. The information presented in this paper aims at significantly reducing the likelihood that your acquisition will fail to deliver on its expected value.

Frontier Strategy Group recently released an exclusive white paper titled, Opportunistic M&A – Upside Potential in a Downturn Environment.

For a copy of the complete white paper in addition to an invitation to an expert led teleconference please fill in your contact details using the form below:

While informal lending is significant, it is not big enough to bring down the entire system.

Trends:

- Informal lending, or shadow banking, has become very active across China since earlier this year

- It has recently caught both media and government attention after multiple cases of “underground trust” went burst

- The situation is worst in Wenzhou, where a number of business owners have gone into hiding or even committed suicide

Drivers:

- A credit tightening policy was implemented by People’s Bank of China in early 2011

- The state-owned banks prefer to lend to state-owned enterprises and large private companies, leaving little credit available to SMEs

- Negative real interest rate and lack of investment choices prompt people to seek a higher return through informal lending

Implications:

- The non-performing loan ratio is going to rise during any economic slowdown, triggering defaults among informal lending entities, many of which are ponzi schemes

- The most risky form of informal lending is curb market lending, where many uninformed individuals and small companies will put money together to lend to highly risky or even “phantom” projects with virtually no due diligence

- The informal lending market is estimated to be one-fifth the size of the total loan market, while the curb market lending is about 1/3 of total informal lending. While these numbers are significant, they are not big enough to bring down the entire system

Trend

Recent policy choices indicate that political considerations are being placed ahead of sound economic management

The central bank’s decision to cut interest rates, despite high inflation and employment, and subsequent intervention to arrest the depreciation of the real has created a tremendous amount of volatility

Industrial policy has become paramount as protectionism leaps into the fore, jeopardizing long-term competitiveness

Import taxes and foreign ownership laws are worsening regulatory uncertainty, leading some companies to rethink investment decisions

By choosing to shelter local producers rather than cut red tape and invest in infrastructure and human capital, the government is further distorting market incentives

Drivers

The government is betting that inflation will decrease as the global economy cools, making growth a higher priority

Financial markets are pricing in an additional 100 basis points worth of cuts to the SELIC rate by the end of the year

Political pressure to address the currency has been building ever since the Dilma administration took office

Dilma is hemmed in by a governing coalition and constitution that makes it difficult to enact long-term reforms to boost competitiveness

Frontier Strategy Group View

The recent spate of pro-inflationary policies poses serious risks to the Brazilian economy, especially given recent demands by workers to raise wages in 2012. If the global economy fails to deteriorate as much as Brazilian officials are expecting, a scenario that is not currently FSG’s base case, inflation could become a major problem

B2C companies selling to low and lower-middle income consumer segments should be wary as inflation reduces the purchasing power of these demographics the most

Are multinational firms undercutting their growth potential in emerging markets because of their incentive systems? While average growth rates across global emerging markets are healthy (14% expected in 2011 from a recent Frontier Strategy Group survey), there does exist a fundamental misalignment between strategy and leadership in these markets. The misalignment is this: the average tenure of an emerging markets leader (typically a regional head of Asia, Latin America or EMEA) is about 3 years – but the average investment in these markets has a payback period much longer-term than that.

Payback periods vary, of course, by industry. But it is not uncommon to hear consumer goods companies, for example, talk about building a brand in a new developing market for several years before they build out their channel. Or for B2B companies to painstakingly build partnerships over the course of several years to set a foundation that will enable them to succeed in certain markets. Yet the vast majority of emerging markets executives (over 80%) are incentivized on short-term financial metrics. A classic case of the folly of rewarding A while hoping for B. Every executive worth his or her salt will do their damnedest to hit the financial targets laid out for them – with the inevitable consequence of compromising the long-term vision that success in emerging markets requires.

The answer clearly lies in tying incentives not just to financial outcomes but also to strategy execution. Companies must walk a fine line here. Clearly, senior executives are used to being told what to get done, not what to do. So the incentives must still be related to achieving outcomes – just not necessarily financial outcomes, which are the most lagging of all success indicators. Recent Frontier Strategy Group research on performance management has uncovered a small but growing trend of companies rewarding executives on strategy execution milestones and other non-financial metrics such as leadership behaviors.

For more detail, please write to me with questions or comments. In a future post – why the corporate budgeting process is the bane of the emerging markets executive’s existence.

In yesterday’s Financial Times, Frontier Strategy Group Director of Global Research Matthew Lasov wrote an article entitled, Emerging Markets: Time is Ripe for Acquisitions. Lasov argues that as managers seek to meet or exceed ambitious growth targets during the next year, the pace of merger and acquisition activity (M&A) in emerging markets is likely to return to and exceed levels last seen in 2007.

The three drivers that will push managers to execute quickly on M&A opportunities are:

- The likelihood of a double-dip recession in developed economies

- Multinationals hold record-high cash reserves

- Scarcity of quality M&A targets in emerging markets

Lasov expands on his analysis in an exclusive Frontier Strategy Group white paper titled, Opportunistic M&A - Upside Potential in a Downturn Environment.

For a copy of the complete white paper in addition to an invitation to an expert led teleconference please fill in your contact details using the form below:

From the housing bubble of 2007 to increased volatility in 2011, the graphic above breaks down the critical events that led to the current global economic instability.

From the housing bubble of 2007 to increased volatility in 2011, the graphic above breaks down the critical events that led to the current global economic instability.

The Turkish lira lost 16% against the dollar in the past 3 quarters and has been one of the worst-performing emerging-market currencies this year. This trend has already started to hit bottom lines and companies are planning to hedge against losses.

There are winners and losers from the lira’s weakness through: local companies and MNCs operating in lira and importing heavy raw materials or parts into Turkey are suffering from rising input costs. On the other hand, companies producing locally and exporting from Turkey are benefitting from Turkey’s stronger export position.

What is causing the lira’s weakness? There are two leading indicators that are driving the lira’s underperformance. First, the country’s rising current account deficit is pressuring Central Bank reserves and the exchange rate. Second, the sovereign debt crisis in Europe is driving investors away from emerging market currencies and toward the dollar, further weakening the lira.

While Turkey’s central bank could hike interest rates to strengthen the lira, the bank has resisted such a move as it would slow down the economy at a time when exports to the EU are already being hit by the sovereign debt crisis. Plus, an exchange rate hike will only be effective if there is exchange rate stability. If the lira is rapidly depreciating against the dollar, interest rate hikes will be seen as a desperate move by the central bank, causing additional portfolio investment flight and further driving down the lira.

As a result, MNCs should anticipate the lira to remain weak through year-end 2012, before appreciating against the dollar in 2013: “The Turkish lira depreciation is not a permanent trend, but a short-to-medium term one,” says Frontier Strategy Group Expert Advisor Kerim Kotan.

Companies producing in Turkey should anticipate lower exchange rate-adjusted costs through next year, while companies selling indirectly to the market should anticipate reduced buying power for dollar-denominated goods. Fahhan Ozcelik, FSG Expert Advisor, also recommends that MNCs operating in Turkey take advantage of the government’s planned incentives for local exporters. One way MNCs can do this is by partnering with local suppliers for semi-finished goods, especially in industries such as textiles, motor vehicles, and electrical machinery.

Featured Authors

-